Affordable Health Insurance Plans: An Overview

The realm of healthcare can often be a labyrinth of expenses, with soaring costs that can leave many feeling lost and overwhelmed. For those navigating life on a budget, the prospect of securing affordable health insurance can seem like an elusive mirage. Yet, there is hope amidst the maze. Affordable health insurance plans serve as a lifeline, offering a beacon of financial relief for individuals and families yearning for peace of mind when it comes to their well-being.

These plans are meticulously crafted to cater to those with limited incomes, ensuring access to essential health services without breaking the bank. They are the embodiment of a healthcare safety net, providing a sturdy foundation to safeguard one’s health amidst life’s unpredictable storms.

Affordable health insurance plans are akin to a prudent investment in one’s future, offering a comforting sense of security against unexpected medical expenses that could potentially derail financial stability. They are the embodiment of a helping hand, guiding individuals and families toward a healthier tomorrow without the burden of overwhelming costs.

In this comprehensive guide, we will delve into the intricacies of affordable health insurance plans, empowering you with the knowledge to make informed decisions about your healthcare. We will explore the types of plans available, their coverage options, eligibility requirements, and the benefits they offer. Armed with this information, you can confidently navigate the healthcare landscape, securing a plan that aligns seamlessly with your needs and budget, ensuring peace of mind for years to come.

Types of Affordable Health Insurance Plans

Navigating the healthcare maze can be daunting, but understanding the types of affordable health insurance plans can serve as a compass, guiding you toward the most suitable option for your unique circumstances.

1. Health Maintenance Organizations (HMOs):

HMOs operate on a network-based model, partnering with specific healthcare providers to offer comprehensive coverage at a fixed monthly premium. The beauty of HMOs lies in their affordability, making them an attractive choice for budget-conscious individuals and families.

2. Preferred Provider Organizations (PPOs):

PPOs grant you the flexibility to seek care from both in-network and out-of-network providers. While out-of-network care may come with higher costs, PPOs offer a wider range of healthcare choices, catering to those who value flexibility over affordability.

3. Exclusive Provider Organizations (EPOs):

EPOs resemble HMOs in their network-centric approach, restricting coverage to a specific network of healthcare providers. However, unlike HMOs, EPOs typically offer lower premiums, making them a cost-effective option for those who prioritize affordability over extensive provider choice.

4. Point-of-Service (POS) Plans:

POS plans strike a balance between HMOs and PPOs, offering a hybrid approach that allows you to seek care from both in-network and out-of-network providers. While out-of-network care may incur higher costs, POS plans provide more flexibility than HMOs, catering to those who seek a compromise between affordability and provider choice.

Coverage Options

Delving into the realm of coverage options is paramount when selecting an affordable health insurance plan. Understanding the scope of services covered empowers you to make informed decisions, ensuring that your plan aligns seamlessly with your healthcare needs.

1. Essential Health Benefits (EHBs):

EHBs form the cornerstone of affordable health insurance plans, mandating coverage for a comprehensive range of essential health services, including preventive care, maternity care, mental health services, and hospitalization.

2. Additional Benefits:

Beyond EHBs, many affordable health insurance plans offer additional benefits to cater to specific needs, such as vision care, dental care, and prescription drug coverage. These add-ons provide a more comprehensive safety net, ensuring that your health is well-protected.

3. Out-of-Pocket Costs:

Out-of-pocket costs refer to the expenses you may incur when utilizing your health insurance plan. These costs can include deductibles, copays, and coinsurance. Understanding these costs is crucial for budgeting and ensuring that your plan aligns with your financial situation.

Eligibility Requirements

Determining your eligibility for affordable health insurance plans is a crucial step in securing coverage. Understanding the eligibility criteria empowers you to navigate the application process with confidence, ensuring that you meet the necessary requirements.

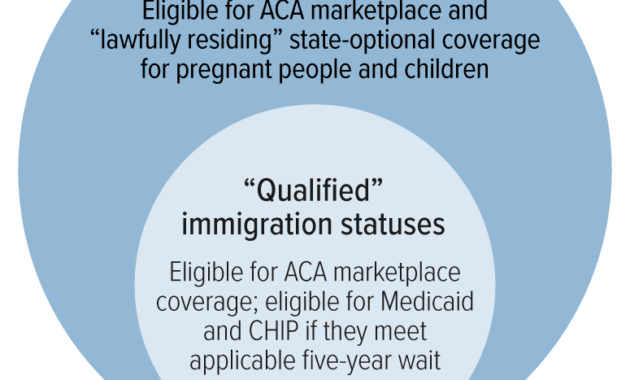

1. Citizenship or Lawful Presence:

To qualify for affordable health insurance plans, you must be a U.S. citizen, a legal resident, or a non-citizen with a qualified immigration status.

2. Income Requirements:

Income plays a significant role in determining your eligibility for affordable health insurance plans. Your income must fall within a specific range to qualify for subsidies and cost-saving measures.

3. State Residency:

Eligibility for affordable health insurance plans may vary depending on your state of residence. Some states have expanded Medicaid eligibility, while others offer their own state-based health insurance programs.

Benefits of Affordable Health Insurance Plans

The benefits of affordable health insurance plans extend far beyond financial savings, offering a multitude of advantages that contribute to your overall well-being.

1. Peace of Mind:

Affordable health insurance plans provide an invaluable sense of peace of mind, knowing that you and your loved ones are protected against unexpected medical expenses.

2. Access to Quality Healthcare:

With affordable health insurance, you gain access to a wide range of healthcare services, ensuring that you receive the necessary medical attention to maintain your health.

3. Preventive Care Coverage:

Affordable health insurance plans often include preventive care coverage, such as screenings and vaccinations, empowering you to take a proactive approach to your health.

4. Chronic Condition Management:

For those managing chronic conditions, affordable health insurance plans provide access to ongoing care and medication, ensuring that your health needs are met.

5. Financial Protection:

Affordable health insurance plans serve as a financial safety net, shielding you from the potentially crippling costs of medical emergencies.

Conclusion

Navigating the healthcare landscape can be a daunting task, but affordable health insurance plans serve as a beacon of hope, providing a pathway to accessible and affordable healthcare for individuals and families with limited incomes. Understanding the types of plans available, coverage options, eligibility requirements, and benefits will empower you to make informed decisions, securing a plan that aligns seamlessly with your needs and budget. Remember, investing in affordable health insurance is an investment in your future well-being, ensuring peace of mind and financial protection for years to come.

What Are Affordable Health Insurance Plans?

Navigating the complex world of health insurance can feel like a daunting task, especially if you’re looking for affordable coverage. But don’t fret! Let’s delve into the world of health insurance and uncover the ins and outs of finding a plan that fits your budget.

Types of Affordable Health Insurance Plans

When it comes to affordable health insurance, there are several options to consider. Let’s explore each type and its potential benefits.

Employer-Sponsored Plans

Employer-sponsored health insurance plans are a common way to obtain coverage. These plans are typically offered by employers to their employees. They are often more affordable than individual plans, as the cost is shared between the employer and employee.

Individual Health Insurance Plans

Individual health insurance plans are purchased directly from an insurance provider. These plans are not tied to an employer, making them a good option for self-employed individuals or those not eligible for employer-sponsored plans. While individual plans can be more expensive than employer-sponsored plans, there are ways to make them more affordable through subsidies and tax credits.

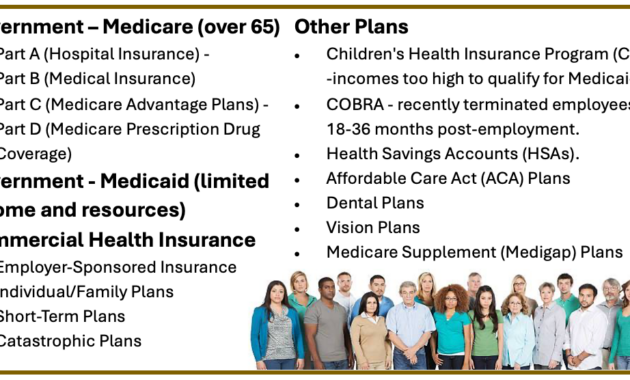

Medicaid

Medicaid is a government-sponsored health insurance program for low-income individuals and families. Medicaid provides comprehensive coverage for a wide range of medical services. If you qualify for Medicaid, it can be an excellent way to obtain affordable health insurance.

Medicare

Medicare is a government-sponsored health insurance program for individuals aged 65 or older, as well as for individuals with certain disabilities. Medicare provides a variety of coverage options, including Part A (hospital insurance), Part B (medical insurance), and Part D (prescription drug coverage).

Affordable Care Act (ACA) Marketplace

The Affordable Care Act (ACA) created a marketplace where individuals and families can shop for and purchase health insurance. The ACA Marketplace offers a variety of plans to choose from, and subsidies and tax credits are available to help make coverage more affordable.

Factors Affecting Health Insurance Affordability

Now that we’ve covered the different types of health insurance plans, let’s dive into the factors that can affect their affordability. Understanding these factors can help you make informed decisions about your coverage.

Age

Age is a significant factor that influences health insurance premiums. Generally, younger individuals pay lower premiums than older individuals. This is because younger people are typically healthier and have a lower risk of needing medical care.

Location

The location where you live can also impact your health insurance premiums. Premiums tend to be higher in urban areas than in rural areas. This is because there are more healthcare providers and facilities in urban areas, which can drive up the cost of care.

Tobacco Use

If you use tobacco, you can expect to pay higher health insurance premiums. This is because tobacco use is a significant risk factor for various health problems, which can lead to higher medical costs.

Health Status

Your health status can also affect your health insurance premiums. If you have a pre-existing condition, you may be charged a higher premium. This is because insurance companies consider individuals with pre-existing conditions to be a higher risk for needing medical care.

Deductible

The deductible is the amount you pay out of pocket before your health insurance coverage kicks in. The higher the deductible, the lower your monthly premium will be. However, a higher deductible means you’ll have to pay more for medical expenses before your insurance starts covering the costs.

Out-of-Pocket Maximum

The out-of-pocket maximum is the most you’ll have to pay for covered medical expenses in a year. This amount includes your deductible, copayments, and coinsurance. The lower the out-of-pocket maximum, the higher your monthly premium will be. However, a lower out-of-pocket maximum can provide peace of mind knowing that you won’t have to pay extensive medical expenses.

Tips for Finding Affordable Health Insurance

Now that you have a better understanding of the factors affecting health insurance affordability, let’s explore some practical tips for finding a plan that fits your budget.

Shop Around

The best way to find an affordable health insurance plan is to shop around and compare quotes from different providers. Don’t be afraid to reach out to multiple insurance companies and get quotes. This will help you understand your options and find the best deal for your needs.

Consider High-Deductible Health Plans (HDHPs)

High-deductible health plans (HDHPs) have lower monthly premiums but higher deductibles. If you’re healthy and don’t expect to need extensive medical care, an HDHP can be a good way to save money on health insurance.

Take Advantage of Subsidies and Tax Credits

If you qualify, you may be eligible for subsidies or tax credits to help make health insurance more affordable. Subsidies are available to individuals and families with low to moderate incomes. Tax credits are available to individuals and families who purchase health insurance through the ACA Marketplace.

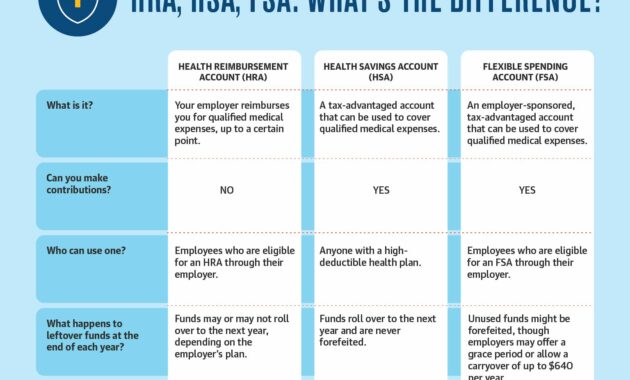

Use a Health Savings Account (HSA)

A Health Savings Account (HSA) is a tax-advantaged savings account that can be used to pay for qualified medical expenses. HSAs are available to individuals who have a high-deductible health plan. Contributions to HSAs are tax-deductible, and withdrawals used for qualified medical expenses are tax-free.

Maximize Your Health Benefits

If you have health insurance, make sure you’re using all of your benefits. This includes preventative care, such as regular checkups and screenings. Preventative care can help catch potential health problems early, which can save you money in the long run.

Conclusion

Finding affordable health insurance doesn’t have to be a daunting task. By understanding the different types of plans available, the factors that affect affordability, and the tips for finding the best deal, you can be well-equipped to make an informed decision about your health insurance coverage.

{kind=link}