Small Business Credit Card Processing Fees

Posted: 02 Apr 2025 on General

Small businesses often rely on credit card payments to process customer transactions. However, there are fees associated with credit card processing that can eat into your profits. Understanding these fees is essential for managing your cash flow and ensuring your business remains profitable.

Types of Credit Card Processing Fees

- Transaction Fees: Per-transaction fees are charged by the credit card network (e.g., Visa, Mastercard) and the payment processor. They typically range from 1.5% to 3.5% of the transaction amount.

- Interchange Fees: These fees are charged by the card-issuing bank to the merchant’s acquiring bank. Interchange fees vary depending on the card type, transaction amount, and cardholder’s country of origin.

- Assessment Fees: Assessment fees are charged by the credit card networks to cover the costs of operating the payment system. These fees are typically a flat amount per transaction, regardless of the amount.

- Chargeback Fees: Chargeback fees are assessed when a customer disputes a transaction and requests a refund. The fees typically range from $15 to $100.

Additional Factors Affecting Credit Card Processing Fees

- Business Volume: Businesses that process higher volumes of transactions may qualify for lower processing fees.

- Card Type: Premium cards (e.g., rewards cards) typically incur higher processing fees than standard credit cards.

- Payment Method: In-person transactions generally have lower processing fees than online or phone transactions.

- Payment Processor: Different payment processors have their own fee structures, so it’s important to compare options before choosing a provider.

Tips for Minimizing Credit Card Processing Fees

- Negotiate lower rates with your payment processor.

- Consider opting for tiered pricing, which charges higher fees for premium cards.

- Encourage customers to use lower-fee payment methods (e.g., debit cards).

- Implement fraud prevention measures to reduce chargebacks.

- Choose a payment processor that offers competitive rates and value-added services.

By understanding the fees associated with credit card processing and taking steps to minimize them, you can optimize your payment processing costs and improve your overall profitability.

Small Business Credit Card Processing Fees: A Comprehensive Guide

In the ever-evolving landscape of business, accepting credit cards has become an indispensable convenience that can streamline transactions and facilitate growth. However, this convenience comes with a price tag: credit card processing fees. For small businesses, these unavoidable charges can have a significant impact on their bottom line.

But understanding these fees is not as daunting as it seems. This comprehensive guide will delve into the intricacies of credit card processing fees, empowering you with the knowledge and strategies to optimize your payment processes and minimize their impact on your business.

What are Small Business Credit Card Processing Fees?

Credit card processing fees are the charges levied by credit card companies and payment processors for handling credit card transactions. They cover the costs associated with authorizing, clearing, and settling payments, as well as the risks involved in accepting credit cards.

These fees typically consist of several components:

- Interchange Fees: These fees are charged by the issuing bank (the bank that issued the customer’s credit card) to the merchant’s bank (the bank that handles the transaction for the merchant).

- Assessment Fees: These fees are charged by credit card networks (e.g., Visa, MasterCard) to cover the costs of running their payment systems.

- Processor Fees: These fees are charged by the payment processor (the company that authorizes and settles the transaction) for their services.

- Gateways Fees: Some merchants may incur additional fees from payment gateways, which facilitate the connection between the merchant and the payment processor.

The interplay of these fees can vary depending on the type of credit card used (e.g., Visa, MasterCard, American Express), the merchant’s industry, and the volume of transactions.

Types of Small Business Credit Card Processing Fees

Small business credit card processing fees come in a variety of forms, each with its unique implications.

- Fixed Fees: These fees are a flat rate per transaction, regardless of the amount.

- Percentage Fees: These fees are a percentage of the transaction amount.

- Tiered Fees: These fees vary based on the type of credit card used and the merchant’s processing volume.

- Monthly Fees: Some payment processors charge a monthly fee for their services.

- PCI Compliance Fees: Merchants may incur fees for complying with Payment Card Industry (PCI) data security standards.

Understanding the different types of fees can help businesses make informed decisions about their payment processing options.

How Small Businesses Can Negotiate Credit Card Processing Fees

While credit card processing fees are an unavoidable cost of doing business, there are strategies that small businesses can employ to negotiate and minimize these fees:

- Shop Around: Compare fees from multiple payment processors to find the most competitive rates.

- Negotiate with Your Processor: Don’t be afraid to negotiate lower fees based on your business’s processing volume and history.

- Consider Surcharging: Some businesses pass on a portion of the credit card processing fees to customers in the form of a surcharge.

- Use a Payment Processor with Transparent Fees: Choose a processor that provides clear and straightforward pricing, without hidden fees.

- Look for Flat-Rate Processing: Flat-rate processing can simplify fee management and make budgeting easier.

By implementing these strategies, small businesses can optimize their credit card processing fees and maximize their profits.

Tips for Minimizing Credit Card Processing Fees for Small Businesses

In addition to negotiating fees, small businesses can employ several tactics to minimize their credit card processing costs:

- Encourage Cash Payments: By offering discounts or incentives for cash payments, businesses can reduce their reliance on credit cards.

- Raise Prices: Consider increasing prices slightly to cover the cost of credit card processing fees.

- Use a Terminal with Multiple Payment Options: Having a terminal that supports various payment methods (e.g., credit cards, debit cards, contactless payments) can reduce the reliance on credit cards with higher fees.

- Monitor Your Fees: Regularly review your payment processor’s statements to identify any discrepancies or excessive fees.

- Stay Up-to-Date on Industry Standards: By keeping abreast of the latest industry trends and technological advancements, businesses can stay informed about new payment processing options and fee structures.

By following these tips, small businesses can effectively manage their credit card processing fees and keep more money in their pockets.

Conclusion

Small business credit card processing fees are an inherent part of accepting credit cards. However, by understanding the components of these fees, negotiating effectively, and implementing cost-saving strategies, businesses can minimize their impact and maintain their financial health. By embracing a proactive approach to payment processing, small businesses can empower themselves to accept credit cards while preserving their profitability.

Small Business Credit Card Processing Fees

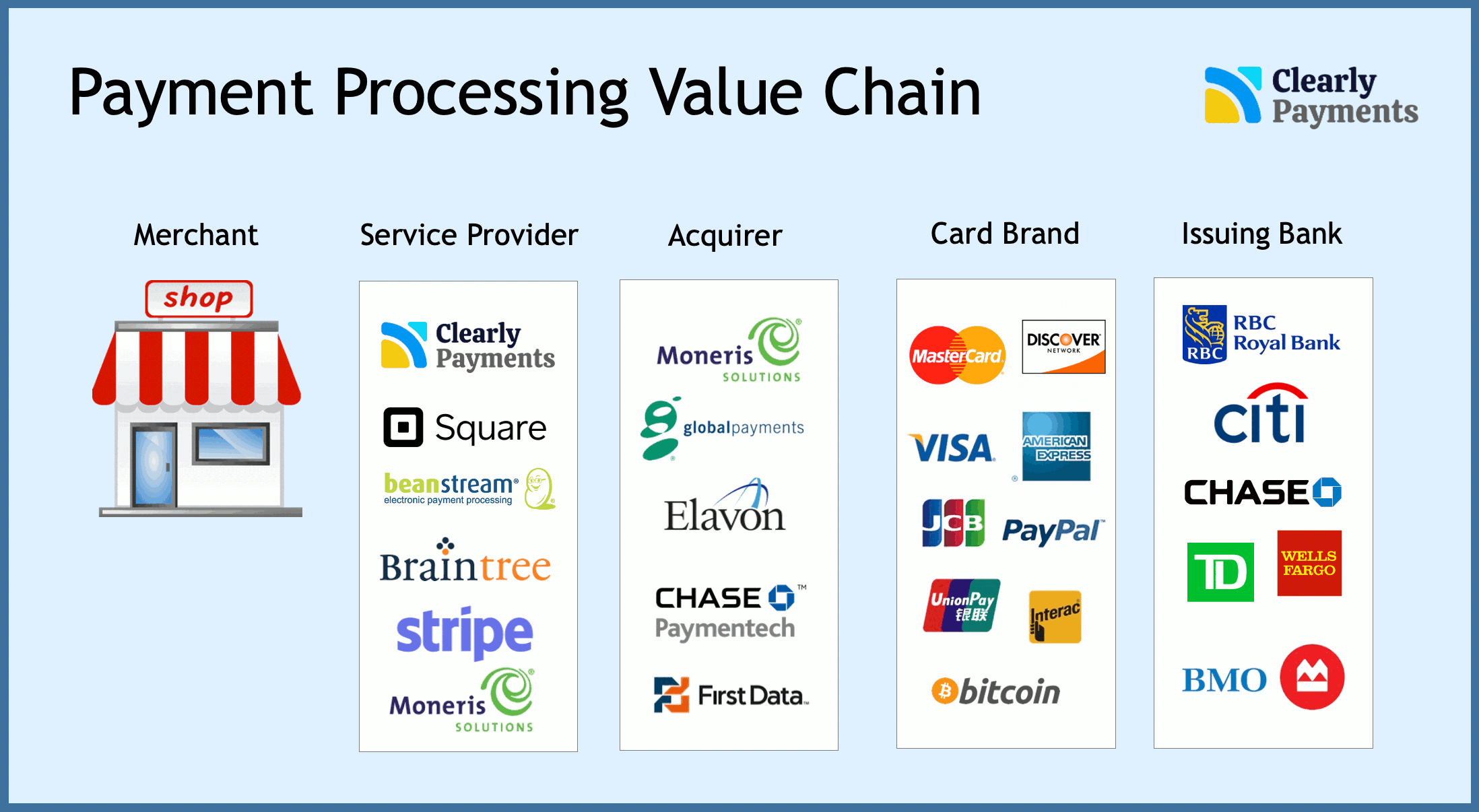

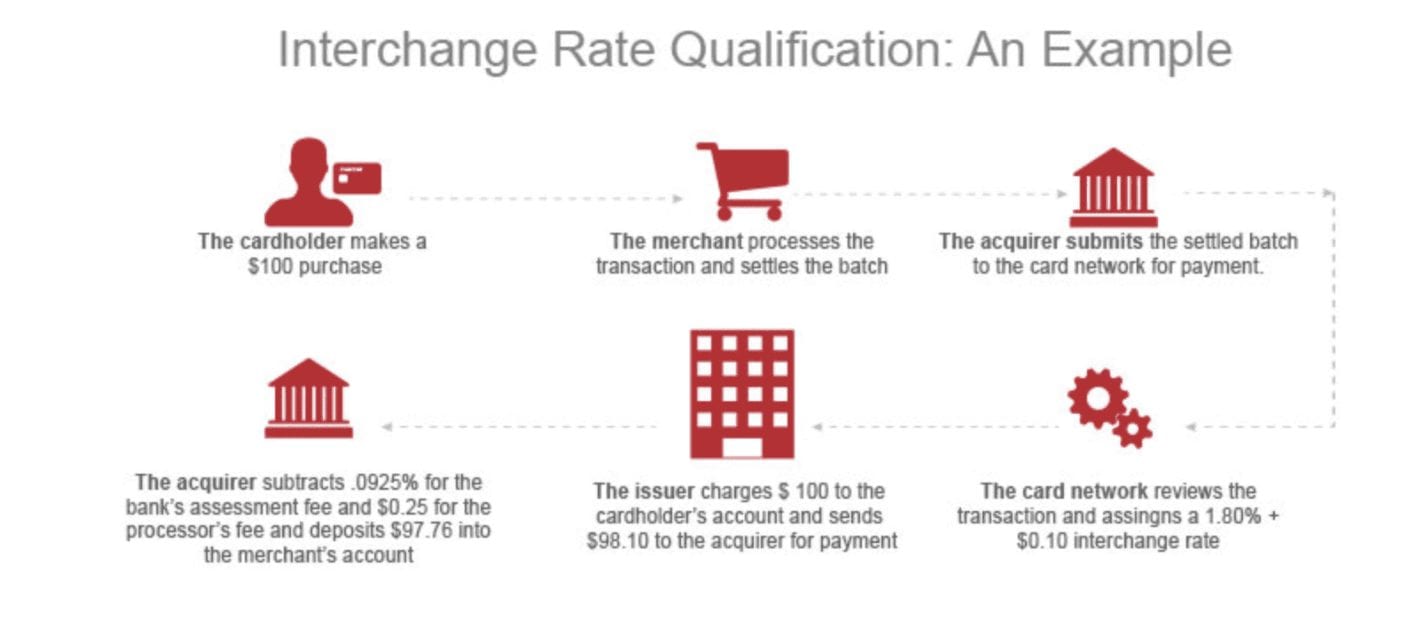

Accepting credit cards is a must for any small business. But with so many different credit card processing companies out there, it can be tough to know which one to choose. And once you’ve chosen a company, you need to be aware of the fees you’ll be paying. The interchange fee is one of the most important fees to understand. Interchange fees are set by the credit card networks (Visa, Mastercard, etc.) and are charged to the merchant every time a customer uses a credit card.

Interchange fees vary depending on a number of factors, including the type of card used, the amount of the transaction, and the merchant’s processing volume. Interchange fees can range from 1% to 3% of the transaction amount, so they can add up quickly. For example, if you process $100,000 in credit card sales per month, you could pay up to $3,000 in interchange fees. Fortunately, there are a number of ways to reduce your interchange fees. One way is to negotiate with your credit card processor. Another way is to choose a processor that offers low interchange rates. You can also reduce your interchange fees by increasing your processing volume.

Types of Credit Cards

There are two main types of credit cards: consumer credit cards and business credit cards. Consumer credit cards are issued to individuals, while business credit cards are issued to businesses. Interchange fees for consumer credit cards are typically higher than interchange fees for business credit cards. This is because consumer credit cards are more likely to be used for personal expenses, which are considered to be higher risk than business expenses.

Transaction Amount

The amount of the transaction also affects the interchange fee. Interchange fees are typically higher for larger transactions. This is because larger transactions are considered to be higher risk than smaller transactions. So, for example, you will pay a higher interchange fee for a $1,000 transaction than you will for a $10 transaction.

Merchant’s Processing Volume

The merchant’s processing volume also affects the interchange fee. Merchants who process a high volume of transactions typically pay lower interchange fees than merchants who process a low volume of transactions. This is because merchants who process a high volume of transactions are considered to be lower risk than merchants who process a low volume of transactions. So, if you process a lot of credit card sales, you are likely to pay lower interchange fees than if you only process a few credit card sales.

Interchange Fees and Your Business

Interchange fees are an important part of the cost of accepting credit cards. By understanding how interchange fees work, you can make informed decisions about which credit card processor to choose and how to reduce your interchange fees. This can help you save thousands of dollars each year.

Small Business Credit Card Processing Fees: A Deep Dive

Running a small business is no walk in the park. There are a million and one things to worry about, from marketing and sales to customer service and inventory management. And on top of all that, you have to deal with the dreaded credit card processing fees. These fees can eat into your profits, so it’s important to understand them before you sign up with a processor.

In this article, we’ll take a deep dive into small business credit card processing fees. We’ll cover everything you need to know, from the different types of fees to how to negotiate the best rates. So sit back, relax, and let’s get started.

Processor Fees

The payment processor charges fees for its services, such as transaction processing, settlement, and customer support. These fees can vary depending on the processor, the type of business, and the volume of transactions.

The most common types of processor fees include:

- Per-transaction fee: This is a flat fee that is charged for each transaction, regardless of the amount.

- Percentage fee: This is a percentage of the transaction amount that is charged by the processor.

- Monthly fee: This is a flat fee that is charged each month, regardless of the number of transactions.

- Annual fee: This is a flat fee that is charged once per year.

In addition to these fees, some processors may also charge additional fees for services such as PCI compliance, chargebacks, and fraud protection.

Negotiating the Best Rates

Now that you understand the different types of processor fees, it’s time to start negotiating the best rates. Here are a few tips:

- Shop around: Don’t just sign up with the first processor you find. Take the time to compare rates from multiple processors before making a decision.

- Negotiate: Once you’ve found a few processors that you’re interested in, don’t be afraid to negotiate. Processors are often willing to give discounts to businesses that are willing to commit to a long-term contract.

- Ask for a statement credit: If you’re not happy with the rates that you’re being offered, ask the processor for a statement credit. This is a one-time payment that can help to offset the cost of processing fees.

By following these tips, you can negotiate the best possible rates on your credit card processing fees.

Other Fees to Consider

In addition to processor fees, there are a number of other fees that you may encounter when processing credit cards. These fees can include:

- Chargeback fees: These fees are charged when a customer disputes a transaction and requests a chargeback. Chargeback fees can vary depending on the processor, but they can be as high as $100 per chargeback.

- Fraud protection fees: These fees are charged to help protect businesses from fraud. Fraud protection fees can vary depending on the processor, but they can be as high as $10 per month.

- PCI compliance fees: These fees are charged to help businesses maintain compliance with the Payment Card Industry Data Security Standard (PCI DSS). PCI compliance fees can vary depending on the processor, but they can be as high as $1,000 per year.

By understanding all of the fees that are associated with credit card processing, you can make an informed decision about which processor to use.

Conclusion

Credit card processing fees can be a significant expense for small businesses. However, by understanding the different types of fees and by negotiating the best possible rates, you can minimize the impact of these fees on your bottom line.

So what are you waiting for? Start comparing rates today and see how much you can save on your credit card processing fees.

Small Business Credit Card Processing Fees: A Comprehensive Guide

In the fast-paced world of business, every penny counts. That’s why it’s crucial for small business owners to understand the ins and outs of credit card processing fees. These fees can add up, especially if you’re not well-informed. But fear not, dear reader! We’ve compiled a comprehensive guide to help you navigate the complexities of credit card processing fees, empowering you to make informed decisions for your business.

Authorization Fees

Imagine this: a customer walks into your store, eager to make a purchase. As you reach for their credit card, a hidden fee lurks in the shadows – the authorization fee. This fee is charged every time a card is authorized for a transaction, regardless of whether it’s ultimately completed. Think of it as a toll fee for the bank’s permission to process the card. Authorization fees typically range from a few cents to a couple of dollars, but they can vary depending on the merchant’s agreement with their payment processor.

Interchange Fees

Now, let’s talk about the big kahuna of credit card processing fees: interchange fees. These fees are levied by the card issuer – the bank that issued the card to the customer – and passed on to the merchant through their payment processor. They usually account for the largest portion of credit card processing costs. Interchange fees are determined by several factors, including the type of card used, the transaction amount, and the merchant’s industry. The more premium the card, the higher the interchange fee. For instance, rewards cards typically have higher interchange fees than basic debit cards.

Assessment Fees

Moving on to assessment fees, which are charged by credit card networks such as Visa, Mastercard, and American Express. These fees represent a percentage of each transaction, typically ranging from 0.1% to 0.2%. They’re collected to help cover the costs of operating the payment networks and ensuring the security of transactions.

Acquirer Fees

Every transaction needs a middleman, and that’s where acquirers come in. Acquirers are financial institutions that process credit card payments on behalf of merchants. They typically charge a fee for their services, which can vary depending on the merchant’s business volume and the type of payment processing solution they use. Acquirer fees can be fixed (a flat rate per transaction) or variable (a percentage of the transaction amount).

Gateway Fees

Think of payment gateways as the gatekeepers of credit card transactions. They connect merchants to the payment networks, enabling secure and efficient processing. Gateway fees vary widely and can include a monthly subscription cost, per-transaction fees, and setup or maintenance fees. The fees depend on the gateway provider and the features offered.

Additional Fees to Watch Out For

There’s more to credit card processing fees than the mainstays we’ve discussed. Keep an eye out for additional fees that can pop up, such as:

- Chargeback fees: When a customer disputes a transaction, merchants may incur fees for processing the chargeback.

- PCI compliance fees: To maintain compliance with Payment Card Industry (PCI) security standards, merchants may need to pay fees for annual audits or software.

- Early termination fees: Breaking a contract with a payment processor before its term ends can result in hefty fees.

- Retrieval request fees: Retrieving transaction records for audits or disputes may incur fees.

- Cross-border transaction fees: Processing payments from customers in different countries can lead to additional fees.

Negotiating and Minimizing Fees

Don’t settle for those hefty fees! Here are a few tips to negotiate and minimize your credit card processing costs:

- Compare fees from multiple processors: Shop around and compare different payment processors to find the best deal.

- Negotiate lower rates: Don’t be afraid to negotiate with your payment processor. If you have a high volume of transactions, you may qualify for discounts.

- Consider tiered pricing: Some processors offer tiered pricing based on transaction volume, so you pay lower fees for higher volumes.

- Choose the right payment methods: Encourage customers to use cards with lower interchange fees, such as debit cards.

- Optimize your checkout process: Reduce abandoned carts and errors to minimize chargeback fees.

Now that you’re armed with this comprehensive guide, you’re equipped to tackle the world of credit card processing fees like a pro. Remember, knowledge is power, especially when it comes to saving your hard-earned money. So, go forth and conquer those fees!

Small Business Credit Card Processing Fees: A Comprehensive Breakdown

In the fiercely competitive landscape of today’s business world, every penny counts. As a small business owner, it’s crucial to understand the ins and outs of credit card processing fees to optimize your cash flow and avoid hefty charges.

Interchange Fees: The Core of the Costs

Interchange fees lie at the heart of credit card processing, accounting for the majority of its costs. These fees are charged by card networks like Visa and Mastercard to facilitate transactions between banks and merchants. The exact rate varies depending on the card type, transaction type, and processing network.

Assessment Fees: A Percentage-Based Bite

In addition to interchange fees, merchants are also subject to assessment fees. These charges, typically ranging from 0.10% to 0.15% of the transaction amount, are imposed by card issuers. They represent a revenue stream for the companies that issue credit cards.

Processor Fees: The Merchant’s Share

Payment processors, such as Square and PayPal, charge fees for their services in enabling credit card transactions. These fees can be either flat rates or tiered, with higher rates applied to larger transactions. It’s essential to compare processors and negotiate the best possible rates.

Gateway Fees: The Bridge Between

Connecting merchants to payment processors, gateways also impose fees for their role in facilitating transactions. Gateway fees can range from a few cents to several dollars per transaction, contributing to the overall processing costs.

PCI Compliance Fees: Protecting Sensitive Data

Businesses handling credit card data must comply with the Payment Card Industry Data Security Standard (PCI DSS) to protect customer information. Compliance requires merchants to implement security measures and undergo regular scanning and certification, which can incur fees.

Additional Fees: The Hidden Costs

Beyond the core fees, merchants may encounter additional charges based on their business model or processing volume. These can include chargeback fees, dispute resolution costs, and fees for advanced features like fraud protection and reporting tools.

Calculating Your Total Costs

Determining your total credit card processing costs can be a complex undertaking. To calculate this figure, consider the various fees discussed above, including interchange, assessment, processor, gateway, PCI compliance, and additional charges. It’s recommended to consult with a payment processor to obtain a customized estimate based on your specific business needs.

Optimizing Your Fees: Strategies for Savings

Savvy small business owners can implement strategies to optimize their credit card processing fees. Here are some tips:

- Negotiate with Processors: Don’t shy away from negotiating with payment processors to secure the most favorable rates.

- Choose the Right Processor: Compare processors to find one that aligns with your business size, transaction volume, and industry.

- Minimize Chargebacks: By implementing robust fraud prevention measures and providing excellent customer service, you can reduce chargebacks and avoid the associated fees.

- Leverage Tiered Pricing: Opt for processors that offer tiered pricing models, which can save you money on smaller transactions.

- Explore Flat Fee Processing: Flat fee processors charge a set fee per transaction, which may be beneficial for businesses with consistent transaction sizes.

Conclusion

Credit card processing fees can be a significant expense for small businesses. By understanding the various fees involved and implementing optimization strategies, business owners can minimize their costs and maximize their profits. Remember, every penny saved is a step towards financial success in the competitive business environment.

Credit Card Processing Fees: A Burden for Small Businesses

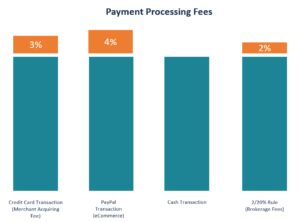

Small businesses are the backbone of our economy, but they often face challenges that larger companies don’t. One of those challenges is the high cost of credit card processing fees. These fees can eat into a small business’s profits and make it difficult to compete with larger businesses. The average small business pays between 2% and 3% in credit card processing fees, which can add up quickly. For example, a small business that processes $100,000 in credit card sales per year could end up paying $2,000 to $3,000 in fees. That’s a lot of money that could be used to invest in the business or hire more employees.

There are a number of factors that affect credit card processing fees, including the type of business, the volume of transactions, and the type of credit card being used. Some businesses are charged higher fees than others, simply because they are considered to be “high risk.” This includes businesses that sell products or services that are often associated with fraud, such as online gambling or adult entertainment. Businesses that process a high volume of transactions are also charged higher fees, because they are seen as being more likely to generate chargebacks. And businesses that accept premium credit cards, such as American Express or Discover, are charged higher fees than those that accept only Visa or Mastercard.

Credit card processing fees are a necessary evil for small businesses, but there are a number of things that businesses can do to reduce their fees. One way to reduce fees is to compare offers from multiple processors. There are a number of different credit card processors out there, and each one offers different rates and fees. By comparing offers, businesses can find the processor that offers the lowest rates and fees for their specific business needs.

Negotiating Credit Card Processing Fees

Another way to reduce fees is to seek volume discounts. Many processors offer discounts to businesses that process a high volume of transactions. Businesses can often negotiate lower rates by simply asking for them. It’s also important to opt for cost-plus pricing models. With cost-plus pricing, businesses are charged a flat fee plus a percentage of each transaction. This type of pricing model is often more cost-effective for businesses that process a high volume of transactions.

Finally, businesses can reduce fees by accepting fewer credit cards. By accepting only the most popular credit cards, businesses can avoid the higher fees that are associated with premium credit cards. Businesses can also encourage customers to use debit cards or cash, which are typically less expensive to process than credit cards.

Credit card processing fees are a challenge for small businesses, but there are a number of things that businesses can do to reduce their fees. By comparing offers, seeking volume discounts, and opting for cost-plus pricing models, businesses can save money on their credit card processing costs.

Additional Tips for Negotiating Credit Card Processing Fees

- Be prepared to walk away. If a processor is unwilling to negotiate, you can always take your business elsewhere.

- Be willing to compromise. You may not be able to get the lowest possible rates, but you should be able to find a processor that offers a fair deal.

- Don’t be afraid to ask for help. There are a number of resources available to help small businesses negotiate credit card processing fees. You can contact your local chamber of commerce, the Small Business Administration, or a credit card processing consultant.

By following these tips, you can reduce your credit card processing fees and save money for your small business.

Small Business Credit Card Processing Fees: A Comprehensive Guide

Credit card processing fees are an unavoidable part of doing business for any small enterprise that accepts plastic. These charges can add up quickly, eating into your profits and making it harder to stay competitive. That’s why small business owners need to understand the different types of fees involved and how to minimize them.

Understanding the Fees

There are a variety of fees associated with credit card processing. Here are some of the most common:

- Transaction fees: This is the percentage of each transaction that you pay to your credit card processor. Fees vary depending on the type of card used (e.g., Visa, Mastercard, Discover) and the amount of the transaction.

- Processing fees: These are fees charged by your credit card processor for the service of processing transactions. Fees typically range from a few cents to a few dollars per transaction.

- Monthly fees: Some credit card processors charge a monthly fee for their services. These fees can range from $10 to $100 or more.

- PCI compliance fees: Payment Card Industry (PCI) compliance is a set of security standards that businesses must follow to protect customer data. Many credit card processors charge fees for helping businesses comply with PCI standards.

How to Minimize Fees

There are several steps you can take to minimize credit card processing fees:

- Negotiate with your processor: Don’t be afraid to negotiate with your credit card processor to get the best possible rates. Be prepared to provide data on your business’s processing volume and history.

- Shop around for the best rates: There are many different credit card processors out there. Take the time to compare rates and fees from multiple processors before choosing one.

- Use a payment gateway: A payment gateway can help you process transactions more efficiently and securely. Payment gateways can also help you reduce fees by allowing you to negotiate better rates with your credit card processor.

- Encourage customers to use debit cards: Debit cards typically have lower processing fees than credit cards. If you offer a discount for customers who use debit cards, you can save money on processing fees and pass the savings on to your customers.

Additional Tips

In addition to the tips above, here are a few additional ways to save money on credit card processing fees:

- Use a flat-rate processor: Flat-rate processors charge a fixed fee per transaction, regardless of the amount of the transaction. This can be a good option for businesses that process a high volume of small-dollar transactions.

- Consider a merchant cash advance: A merchant cash advance is a type of financing that allows you to receive a lump sum of money upfront. The advance is then repaid through a percentage of your daily credit card sales. Merchant cash advances can be a good option for businesses that need quick access to funds.

- Contact your trade association: Your trade association may be able to provide you with resources and discounts on credit card processing fees.

Conclusion

Credit card processing fees are a necessary cost of doing business. However, there are several steps you can take to minimize these fees and maximize your profits. By understanding the different types of fees involved and how to negotiate the best possible rates, you can save money on credit card processing and keep more of your hard-earned revenue.

Share this:

Related Articles

Standard Credit Card Processing Fees Explained

02 Apr 2025

Understanding Vagaro Credit Card Processing Fees

02 Apr 2025

What Are Credit Card Processing Fees?

02 Apr 2025

{kind=link}

Chase Bank Credit Card Processing Fees

02 Apr 2025