Lowest Credit Card Processing Fees For Small Businesses

Posted: 02 Apr 2025 on General

The Lowest Credit Card Processing Fees for Small Businesses

Small businesses seeking to minimize their payment processing expenses should prioritize selecting the appropriate credit card processor. With numerous providers offering a wide range of fee structures, navigating this landscape can be challenging. This comprehensive guide will provide valuable insights into the lowest credit card processing fees available, empowering small businesses to make informed decisions that optimize their financial performance.

Factors Influencing Credit Card Processing Fees

Several factors influence the fees associated with credit card processing, including:

- Transaction Volume: Processors often offer tiered pricing based on the number of transactions processed monthly. Higher transaction volumes typically result in lower per-transaction fees.

- Card Type: Different card types (e.g., Visa, Mastercard) have varying interchange fees, which are passed on to merchants by processors.

- Processing Method: Swipe, chip, and contactless transactions generally incur different fees due to variations in security measures and equipment requirements.

- Business Model: Industries with high chargeback rates or specialized payment needs may face higher fees.

- Processor Fees: Each processor has its own fee structure, including monthly fees, setup fees, and per-transaction charges.

Lowest Credit Card Processing Fees for Small Businesses

Numerous credit card processors cater to small businesses, offering competitive fee structures and tailored solutions. Here are some of the providers with the lowest fees:

- Square: Known for its low flat-rate pricing, Square charges 2.6% + 10¢ per transaction for in-person payments and 2.9% + 30¢ for online transactions.

- Stripe: Another popular option, Stripe offers a flat fee of 2.9% + 30¢ per transaction for both in-person and online payments.

- PayPal: PayPal’s standard fees include 3.49% + 49¢ per transaction for in-person payments and 2.9% + 30¢ for online payments.

- Clover: Clover provides a range of fee structures depending on the type of payment processing solution required, with some options starting at 1.3% + 10¢ per transaction.

Additional Tips for Lowering Credit Card Processing Fees

Beyond choosing a processor with low fees, small businesses can further reduce their payment processing expenses by:

- Negotiating Interchange Fees: Some processors allow businesses to negotiate interchange fees with their issuing banks.

- Offering Rewards Points: Providing loyalty or rewards programs can incentivize customers to use their cards, generating additional revenue that can offset processing costs.

- Optimizing Transaction Volumes: Consolidating payments and increasing transaction volume can qualify businesses for lower tier pricing.

- Avoiding Chargebacks: Businesses should implement measures to minimize chargebacks, as they can incur high fees.

Conclusion

By carefully considering the factors influencing credit card processing fees and selecting a provider with competitive rates, small businesses can minimize their payment processing expenses and maximize their profitability. By following these insights and implementing the additional tips provided, businesses can gain a competitive edge in today’s dynamic business environment.

Lowest Credit Card Processing Fees for Small Businesses

As a small business owner, you know every penny counts. That’s why finding the lowest credit card processing fees is crucial to keeping your business afloat. The good news is, there are several options to choose from, each with its own set of pros and cons. Let’s dive right in and explore the lowest credit card processing fees for small businesses.

Interchange-Plus Pricing: Breaking Down the Details

Interchange-plus pricing is a transparent fee structure that has gained popularity among small businesses. It involves two components: the interchange fee and the markup. The interchange fee is a fee charged by the card network (Visa, Mastercard, etc.) for each transaction. The markup is the additional fee charged by your payment processor.

The beauty of interchange-plus pricing lies in its transparency. You can easily calculate your total processing fees by adding the interchange fee and the markup. This allows you to compare pricing between different processors and negotiate the best deal for your business.

Here’s an example to illustrate interchange-plus pricing: Suppose the interchange fee for a $100 transaction is 2.5%. If your payment processor charges a 0.5% markup, your total processing fee would be 3%. This means you would pay $3 for processing the $100 transaction.

Interchange-plus pricing is ideal for businesses that process a high volume of small-ticket transactions, as it offers lower fees compared to flat-rate pricing. However, businesses that process large-ticket transactions may find interchange-plus pricing to be more expensive.

When considering interchange-plus pricing, it’s important to compare the markups charged by different payment processors. The lower the markup, the lower your processing fees will be.

Overall, interchange-plus pricing provides transparency and flexibility, making it a viable option for small businesses seeking the lowest credit card processing fees.

Navigating the Labyrinth of Credit Card Processing Costs: Uncovering the Lowest Fees for Small Businesses

In the competitive landscape of small business, every penny counts. Credit card processing fees can quickly chip away at your hard-earned profits, making it essential to find the most cost-effective solutions. This guide will delve into the nuances of credit card processing fees, unveiling the secrets to securing the lowest rates.

Flat-Rate Processing: A Simple, Predictable Option

Flat-rate processing offers a straightforward approach to transaction fees, charging a fixed percentage per swipe. This model eliminates the complexity of tiered pricing and interchange fees, providing a clear and predictable cost structure. It’s an ideal solution for businesses with a high volume of low-value transactions, such as retail stores or service providers.

Interchange Fees: Breaking Down the Interbank Shuffle

Interchange fees, also known as swipe fees, are the charges incurred by the credit card issuer and payment processor every time a card is used. These fees vary based on the type of card, transaction type, and processing network. Understanding interchange fees is crucial for optimizing your payment strategy.

Understanding Tiered Pricing: A Maze of Surcharges

Tiered pricing introduces a level of complexity to credit card processing. This model assigns transactions to different tiers based on criteria such as card type, transaction size, and merchant category code (MCC). Each tier carries its own set of interchange fees and markup rates, making it essential to analyze your transaction patterns to identify the most cost-effective tier structure.

Membership Fees: The Hidden Cost of Exclusive Clubs

Some payment processors offer membership programs that charge a fixed monthly or annual fee in exchange for lower processing rates. These fees can add up over time, especially for businesses with low transaction volumes. Carefully weigh the potential savings against the membership cost to determine if it’s a worthwhile investment.

Extracting the Lowest Fees: A Step-by-Step Guide

- Shop Around: Compare rates from multiple processors to find the most competitive deals. Don’t settle for the first quote you receive.

- Negotiate: Once you’ve identified a few potential processors, don’t hesitate to negotiate rates. Small businesses have the power to negotiate favorable terms, especially if they offer a high volume of transactions.

- Reduce Interchange Fees: Analyze your transactions and identify ways to reduce interchange fees. This may involve switching to lower-tier cards or negotiating with your suppliers to reduce transaction sizes.

- Consider Cash Discounts: Offering a cash discount can incentivize customers to pay without using credit cards, reducing your processing costs significantly.

- Monitor Regularly: The credit card processing landscape is constantly evolving. Stay informed about industry trends and regularly review your processing fees to ensure you’re getting the best deal.

Lowest Credit Card Processing Fees for Small Businesses

Every business wants to keep their costs down, and small businesses are no exception. Credit card processing fees can be a significant expense, so it’s important to understand the different types of fees and how to find the lowest rates. In this article, we’ll discuss the lowest credit card processing fees for small businesses and provide tips on how to find the best deal.

The lowest credit card processing fees for small businesses are typically found with interchange-plus pricing. Interchange-plus pricing passes the interchange fee set by credit card networks on to the merchant, plus a markup. This pricing model is ideal for businesses that process large transactions.

In addition to interchange-plus pricing, there are a number of other factors that can affect your credit card processing fees. These include:

- The type of business you have.

- The average transaction amount.

- The number of transactions you process each month.

It’s important to compare quotes from multiple credit card processors before making a decision. Be sure to ask about all of the fees involved, including the interchange fee, markup, and any other monthly or annual fees.

Flat-Rate Pricing

Flat-rate pricing is a simple pricing model that charges a fixed fee per transaction, regardless of the transaction amount. This pricing model is ideal for businesses that process a lot of small transactions.

The flat-rate fee will typically be higher than the interchange fee, but it’s easier to budget for. Flat-rate pricing can also be a good option for businesses that process a mix of small and large transactions.

Tiered Pricing

Tiered pricing is a pricing model that charges different rates for different types of transactions. For example, you may be charged a lower rate for debit card transactions than for credit card transactions.

Tiered pricing can be a good option for businesses that process a lot of different types of transactions. However, it’s important to be aware of the different rates that you’ll be charged.

Membership Pricing

Membership pricing is a pricing model that charges a monthly or annual fee in addition to the processing fees. This pricing model can be a good option for businesses that process a lot of transactions each month.

The membership fee will typically be higher than the fees charged under other pricing models, but the overall cost may be lower if you process a lot of transactions.

Which Pricing Model Is Right for You?

The best pricing model for your business will depend on a number of factors, including the type of business you have, the average transaction amount, and the number of transactions you process each month.

If you’re not sure which pricing model is right for you, contact a credit card processor and ask for a quote.

Lowest Credit Card Processing Fees for Small Businesses: A Comprehensive Guide

In today’s digital age, accepting credit cards has become indispensable for small businesses. But with a plethora of credit card processors vying for your attention, choosing the one with the lowest fees can be a daunting task. This comprehensive guide will shed light on the intricacies of credit card processing fees and help you navigate the complexities of this essential business expense.

Understanding the Credit Card Processing Fee Structure

The credit card processing fee structure typically consists of three components:

-

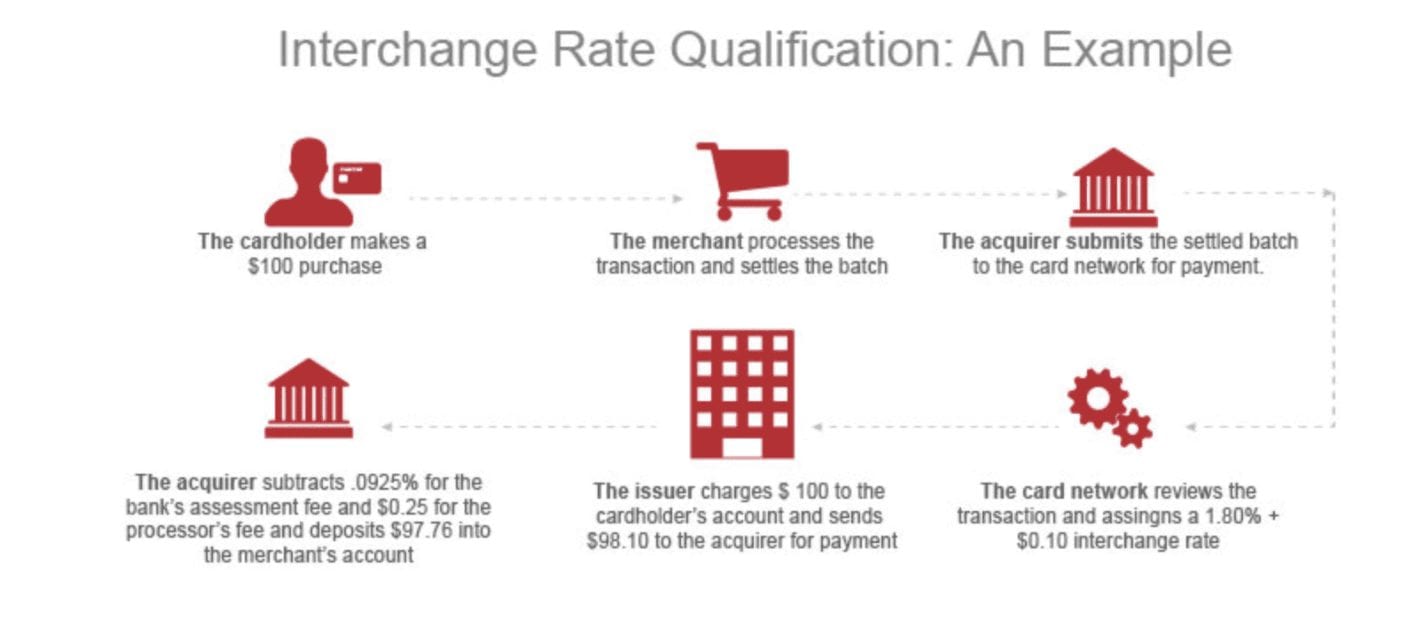

Interchange Fee: This fee is charged by the credit card network (e.g., Visa, Mastercard) to the merchant’s bank. It covers the network’s costs associated with processing the transaction.

-

Assessment Fee: This fee is imposed by the credit card issuing bank to the merchant’s bank. It represents the bank’s profit margin for issuing the card.

-

Processing Fee: This fee is charged by the credit card processor for providing the necessary technology and support for processing the transaction.

Flat-Rate Pricing vs. Tiered Pricing

Credit card processors generally offer two pricing models: flat-rate pricing and tiered pricing.

1. Flat-Rate Pricing:

With flat-rate pricing, merchants pay a single, fixed fee for all transactions, regardless of the type or volume of transaction. This model is suitable for businesses with predictable transaction patterns and relatively low transaction volumes.

2. Tiered Pricing:

Tiered pricing divides transactions into categories (qualified, mid-qualified, and non-qualified) and charges varying fees based on the tier. This structure is appropriate for businesses with a mix of high-value and low-value transactions.

Interchange Categories and Fees

Interchange fees vary based on the type of transaction and the merchant’s industry. The International Organization for Standardization (ISO) has established four interchange categories, each with its own fee structure.

-

Category 1: Includes low-risk transactions from traditional brick-and-mortar stores.

-

Category 2: Covers card-not-present transactions (e.g., online purchases) and purchases from high-risk industries.

-

Category 3: Encompasses government and travel-related transactions.

-

Category 4: Includes cash advances and balance transfers.

Evaluating Credit Card Processing Fees

When evaluating credit card processing fees, small businesses should consider the following factors:

-

Volume of Transactions: Businesses with higher transaction volumes may benefit from flat-rate pricing, while tiered pricing may be more cost-effective for those with lower volumes.

-

Average Transaction Size: Businesses with high-value transactions may incur higher fees with tiered pricing, making flat-rate pricing a more attractive option.

-

Interchange Category: Businesses in high-risk industries or those that frequently process card-not-present transactions should expect higher interchange fees.

Negotiating Lower Fees

Don’t hesitate to negotiate lower fees with potential credit card processors. Some strategies to consider include:

-

Shop Around: Compare offers from multiple processors to find the best deal.

-

Bundle Services: Consider combining credit card processing with other services (e.g., merchant accounts, payment gateways) to receive a bundled discount.

-

Provide Historical Data: Share your historical transaction data to demonstrate your processing volume and average transaction size, which can strengthen your negotiating position.

The Ultimate Guide to Choosing Credit Card Processing Fees for Your Small Business

Navigating the complex world of credit card processing can be a daunting task for small business owners. With a myriad of providers and fee structures, deciphering the lowest rates can be like searching for a needle in a haystack. However, understanding the ins and outs of processing fees can lead you to significant savings that can bolster your bottom line. In this comprehensive guide, we’ll unravel the hidden fees to watch out for, explore the factors affecting processing costs, and present a list of the lowest credit card processing fees for small businesses, empowering you to make informed decisions that drive profitability.

Understanding Credit Card Processing Fees

When a customer swipes their plastic, a series of behind-the-scenes transactions occur, each carrying a fee. These fees are typically a combination of interchange fees, assessment fees, and processor fees. Interchange fees are set by the card networks (Visa, MasterCard, etc.) and vary based on the type of card used and the transaction amount. Assessment fees are levied by the card networks to cover the cost of processing the transaction. Processor fees are charged by the company handling the transaction and can vary significantly depending on the provider.

Factors Affecting Processing Costs

Several factors influence the processing fees you’ll pay, including:

- Card type: Premium cards, such as rewards cards, typically have higher interchange fees than standard cards.

- Transaction type: In-person transactions generally have lower fees than online or phone transactions.

- Monthly transaction volume: Higher transaction volumes often qualify for lower fees due to economies of scale.

- Processor markup: Different processors charge different markups on top of the interchange and assessment fees.

Lowest Credit Card Processing Fees for Small Businesses

Finding the lowest credit card processing fees for your small business requires careful comparison. Based on industry research and analysis, here are some of the most competitive options:

- Square: Known for its simplicity and affordable rates, Square offers interchange-plus pricing with no hidden fees. For qualified businesses, processing fees can be as low as 2.6% + 10¢ per transaction.

- PayPal: A popular choice for online businesses, PayPal charges a flat rate of 2.9% + 30¢ per transaction. For high-volume businesses, PayPal offers custom pricing options.

- Stripe: A leading payment gateway used by many small businesses, Stripe offers tailored pricing based on transaction volume. For low-volume businesses, processing fees can be as low as 2.9% + 30¢ per transaction.

- Clover: Clover provides POS systems and payment processing solutions. Its fees vary depending on the type of equipment and services used but typically range from 2.75% + 9¢ to 3.5% + 15¢ per transaction.

- Helcim: A Canadian payment processor known for its transparent pricing, Helcim offers interchange-plus pricing with no monthly fees or PCI compliance fees. Processing fees typically range from 2.49% + 10¢ to 3.49% + 15¢ per transaction.

Hidden Fees to Watch Out For

Beware of additional fees that can inflate overall processing costs, such as:

- PCI compliance fees: Some processors charge a monthly fee to ensure your business complies with Payment Card Industry (PCI) security standards.

- Chargeback fees: If a customer disputes a transaction, you may be charged a fee by the processor.

- Monthly minimums: Certain processors require you to process a minimum amount of transactions each month or face a penalty fee.

Negotiating Lower Processing Fees

As a small business owner, you can negotiate lower processing fees by:

- Shopping around: Compare quotes from multiple providers to find the best rates.

- Bundling services: Some processors offer discounts if you bundle payment processing with other services, such as POS systems or merchant accounts.

- Increasing transaction volume: Higher transaction volumes can qualify you for lower rates.

Conclusion

Navigating the world of credit card processing fees can be tricky, but it’s essential for small businesses to understand their options and make informed decisions. By being aware of the factors affecting processing costs, negotiating lower fees, and avoiding hidden expenses, you can significantly reduce your processing costs and increase profitability. Remember, the lowest credit card processing fees for your business will depend on your specific needs and circumstances. So, take the time to research and compare providers to find the solution that best meets your requirements.

The Search for the Lowest Credit Card Processing Fees for Small Businesses

In a bustling marketplace where every penny counts, small businesses are perpetually on the lookout for ways to streamline their operations and keep costs down. Credit card processing fees can represent a significant expense, potentially eating into hard-earned profits. But fear not, intrepid entrepreneurs, for there are ways to minimize these fees and give your bottom line a much-needed boost.

Seek Out the Most Competitive Rates

Don’t settle for the first processing company that comes along. Shop around, compare quotes, and negotiate with potential providers. Remember, it’s not just about the headline fee; inquire about any hidden costs or additional charges that could creep up down the road. Transparency is key here.

Embrace the Power of Multiple Payment Methods

Don’t limit your customers to one or two payment options. By accepting a wider range of cards, including Visa, Mastercard, American Express, and Discover, you increase your chances of capturing every sale. Of course, each payment method may have different processing fees, so be sure to factor that into your decision-making.

Implement Chargeback Prevention Measures

Chargebacks can be a costly headache for businesses. When a customer disputes a transaction, the processor typically reverses the charges, leaving you out of pocket. To avoid this unpleasant scenario, implement measures to minimize chargebacks. Clear communication with customers, a user-friendly checkout process, and robust fraud detection systems can all help.

Tips for Minimizing Fees

Now that we’ve covered the basics, let’s delve into some more specific strategies for cutting credit card processing fees:

1. Negotiate with Processors

Don’t be afraid to ask for a lower rate. Many processors are willing to negotiate, especially if you’re a high-volume merchant. Be prepared to provide data on your transaction history and show them why you’re a valuable customer.

2. Accept Multiple Payment Methods

As mentioned earlier, offering multiple payment options can help you reduce fees. Some processors charge higher rates for certain card types, so by accepting a wider range of cards, you can spread out your costs.

3. Implement Measures to Reduce Chargebacks

Chargebacks are a major pain for businesses. Not only do you have to refund the customer, but you may also be charged a processing fee. To reduce chargebacks, make sure your checkout process is clear and easy to understand, and implement fraud detection measures to identify and prevent fraudulent transactions.

4. Set Up Recurring Billing

If you have customers who pay you on a regular basis, consider setting up recurring billing. This can help you reduce processing fees, as most processors charge lower rates for recurring transactions.

5. Consider a Flat-Rate Processor

Flat-rate processors charge a single, fixed fee for all transactions, regardless of the amount or card type. This can be a good option for businesses that have a high volume of low-value transactions.

6. Use a Payment Gateway

A payment gateway allows you to accept credit card payments online. Some payment gateways charge processing fees, but others offer free or low-cost plans. Be sure to compare the fees and features of different payment gateways before choosing one.

7. Considerations for High-Volume Merchants

If you’re a high-volume merchant, you may be able to negotiate even lower processing fees. Some processors offer tiered pricing, which means that the more transactions you process, the lower your rate will be. You may also be able to negotiate a custom rate with your processor.

Share this:

Related Articles

Standard Credit Card Processing Fees Explained

02 Apr 2025

Understanding Vagaro Credit Card Processing Fees

02 Apr 2025

What Are Credit Card Processing Fees?

02 Apr 2025

{kind=link}

Chase Bank Credit Card Processing Fees

02 Apr 2025