Introduction

If you’re searching for cheap health insurance coverage in Texas, there are multiple options to consider. The Lone Star State’s insurance market is highly competitive, with numerous providers offering a wide range of plans to suit diverse needs and budgets. Whether you’re an individual, a family, or a small business owner, finding affordable health insurance in Texas is entirely possible.

Navigating the healthcare landscape can be daunting, especially when it comes to understanding insurance plans and comparing costs. This comprehensive guide aims to simplify the process. We’ll explore the different types of health insurance plans available in Texas, provide tips for finding affordable coverage, and highlight resources to help you make informed decisions about your healthcare needs.

Types of Health Insurance Plans in Texas

There are two primary types of health insurance plans available in Texas: Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). HMOs typically offer lower monthly premiums but require you to use healthcare providers within their network. PPOs provide more flexibility in choosing providers but come with higher premiums.

In addition to these two main types, there are also other health insurance options available, including:

- Exclusive Provider Organizations (EPOs)

- Point-of-Service (POS) plans

- High-Deductible Health Plans (HDHPs)

Each type of plan has its own advantages and disadvantages. It’s crucial to carefully consider your healthcare needs and budget when selecting a plan that’s right for you.

Finding Affordable Health Insurance in Texas

Finding affordable health insurance in Texas doesn’t have to be a headache. Here are some tips to help you save money on your coverage:

- Shop around. Compare quotes from multiple insurance companies to ensure you’re getting the best deal. Online insurance marketplaces can make this process easier.

- Consider your deductible. A higher deductible can lower your monthly premium, but it also means you’ll pay more out-of-pocket for medical expenses before your insurance kicks in.

- Take advantage of tax credits and subsidies. The Affordable Care Act provides financial assistance to eligible individuals and families to help them afford health insurance. Explore these options to see if you qualify.

Don’t hesitate to reach out to an insurance agent or broker for guidance. They can provide personalized recommendations and help you find the most affordable health insurance plan in Texas that meets your needs.

Resources for Finding Affordable Health Insurance in Texas

Several resources are available to help you find affordable health insurance in Texas:

- Texas Health Insurance Marketplace: This online platform allows you to compare plans and enroll in coverage. You may qualify for financial assistance through the Marketplace.

- Texas Department of Insurance (TDI): TDI regulates the insurance industry in Texas and provides information and resources on health insurance.

- Nonprofit organizations: Many nonprofit organizations offer free or low-cost health insurance counseling and enrollment services.

By utilizing these resources, you can increase your chances of securing affordable health insurance coverage in Texas.

Conclusion

Finding affordable health insurance in Texas is achievable with the right knowledge and resources. By understanding the different types of plans available, comparing costs, and taking advantage of available assistance, you can protect your health without breaking the bank. Remember, having health insurance is not just a financial decision; it’s an investment in your well-being and peace of mind.

Affordable Health Insurance Plans in Texas: Navigating the Maze

In the Lone Star State, accessing affordable health insurance can feel like a daunting task. With a vast array of plans and providers, finding the right coverage that fits your budget and needs can be a challenge. This comprehensive guide will unravel the complexities of the Texas health insurance landscape, empowering you to make informed decisions about your healthcare.

Types of Affordable Health Insurance Plans in Texas

Texas offers a multitude of affordable health insurance options to meet the diverse needs of its residents. Understanding the different types of plans available is crucial for making the best choice for your situation.

Employer-Sponsored Plans

For many Texans, employer-sponsored health insurance is the most common and affordable option. These plans are typically offered by businesses with 50 or more employees and provide a range of coverage options, from basic to comprehensive. Employees may contribute a portion of the premium, while the employer often covers the remaining costs. The benefits and costs of employer-sponsored plans vary depending on the size and industry of the company.

Individual Plans

For individuals who do not have access to employer-sponsored coverage, the Health Insurance Marketplace (also known as the "Affordable Care Act") offers a wide selection of individual plans. These plans are designed to cater to a range of incomes and provide financial assistance to those who qualify. Individuals can enroll in an individual plan during the annual open enrollment period, which typically runs from November 1st to January 15th.

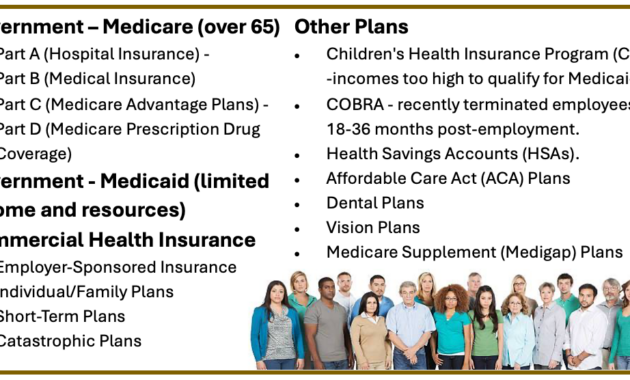

Medicaid and CHIP

Medicaid and the Children’s Health Insurance Program (CHIP) are government-funded health insurance programs for low-income individuals and families. These programs provide comprehensive coverage for a range of healthcare services, including doctor visits, hospital stays, and prescription drugs. Eligibility for Medicaid and CHIP is based on factors such as income, family size, and age.

Selecting the Right Plan for You

Choosing the right health insurance plan involves evaluating your individual needs, considering factors such as:

- Coverage: Determine the types of healthcare services you need covered, such as doctor visits, hospital stays, and prescription drugs.

- Premiums: Consider the monthly cost of the plan and how it fits within your budget.

- Deductibles: A deductible is the amount you pay out of pocket before the insurance coverage begins. Choose a plan with a deductible that you are comfortable paying.

- Copayments and Coinsurance: These are the fixed amounts you pay for specific healthcare services, such as doctor visits or prescription drugs. Compare these costs between different plans.

- Provider Network: Ensure that the plan you choose includes healthcare providers in your area.

- Prescription Drug Coverage: If you rely on prescription medications, check the plan’s coverage for the drugs you need.

Navigating the world of health insurance can be overwhelming, but by understanding the different types of plans available and carefully considering your individual needs, you can find an affordable and comprehensive coverage that meets your requirements. Stay tuned for future articles in this series, where we will delve deeper into specific plan options and provide tips for maximizing your health insurance benefits.

Affordable Health Insurance Plans in Texas

Navigating the healthcare landscape can be a daunting task, especially when it comes to finding affordable health insurance plans. In Texas, there are a plethora of options available, each with its own set of benefits and drawbacks. Whether you’re an individual, a family, or an employer, understanding the different types of plans and their associated costs is crucial for making an informed decision. In this comprehensive guide, we delve into the world of health insurance in Texas, exploring the various plans available and providing tips on how to find the most affordable option that meets your needs.

Texas is home to a diverse population with varying healthcare needs. The state has a higher-than-average uninsured rate compared to other states, highlighting the importance of accessible and affordable health insurance. With the passage of the Affordable Care Act (ACA), also known as Obamacare, millions of Texans gained access to health insurance coverage. However, the ACA’s fate remains uncertain, leaving many wondering about the future of health insurance in the state. Despite the uncertainties, there are still a number of affordable health insurance plans available in Texas. These plans offer a range of benefits, including preventive care, doctor visits, hospital stays, and prescription drug coverage.

When searching for affordable health insurance plans in Texas, it’s essential to compare quotes from multiple providers. This can be done through online marketplaces, such as the Health Insurance Marketplace, or by contacting insurance companies directly. It’s also important to consider your individual needs and budget when choosing a plan. Factors such as age, health status, and income can all impact the cost of health insurance. By taking the time to research and compare plans, you can find the most affordable option that meets your specific requirements.

Employer-Sponsored Plans

Employer-sponsored plans are offered by employers to their employees. These plans can be a good option if your employer offers them, as they are often more affordable than individual plans. Employer-sponsored plans typically offer a variety of benefits, including health, dental, vision, and prescription drug coverage. The cost of these plans is typically shared between the employer and the employee, with the employer paying a larger portion. Employer-sponsored plans can be a good way to save money on health insurance, but they are not always the best option for everyone. If you are not eligible for an employer-sponsored plan, or if the plan offered by your employer does not meet your needs, you may want to consider purchasing an individual health insurance plan.

Individual Health Insurance Plans

Individual health insurance plans can be purchased by individuals who do not have access to employer-sponsored plans. These plans are typically more expensive than employer-sponsored plans, but they offer more flexibility. Individual health insurance plans allow you to choose your own doctor and hospital, and you can customize your plan to meet your specific needs. However, individual health insurance plans can be more expensive than employer-sponsored plans, and they may not offer the same level of benefits. If you are considering purchasing an individual health insurance plan, it is important to compare quotes from multiple providers and to carefully consider your needs and budget.

Government-Sponsored Health Insurance Plans

Government-sponsored health insurance plans are available to low-income individuals and families. These plans are typically more affordable than employer-sponsored plans or individual health insurance plans. Government-sponsored health insurance plans include Medicaid and the Children’s Health Insurance Program (CHIP). Medicaid is a health insurance program for low-income individuals and families. CHIP is a health insurance program for children from low-income families. Both Medicaid and CHIP offer a variety of benefits, including health, dental, vision, and prescription drug coverage. If you are eligible for Medicaid or CHIP, these programs can provide you with affordable health insurance coverage.

Tips for Finding Affordable Health Insurance Plans in Texas

Finding affordable health insurance plans in Texas can be a challenge. However, there are a few things you can do to make the process easier. First, compare quotes from multiple providers. This can be done through online marketplaces, such as the Health Insurance Marketplace, or by contacting insurance companies directly.

Second, consider your individual needs and budget when choosing a plan. Factors such as age, health status, and income can all impact the cost of health insurance. By taking the time to research and compare plans, you can find the most affordable option that meets your specific requirements.

Finally, don’t be afraid to ask for help. There are many resources available to help you find affordable health insurance plans in Texas. You can contact the Health Insurance Marketplace for assistance, or you can talk to a health insurance agent or broker. These professionals can help you compare plans and find the best option for your needs.

Conclusion:

Finding affordable health insurance plans in Texas can be a challenge, but it is possible. By following these tips, you can find the right plan for your needs and budget. With the right plan, you can protect yourself from unexpected medical expenses and ensure that you have access to the healthcare you need.

Affordable Health Insurance Plans in Texas: A Comprehensive Guide

The Lone Star State offers a diverse range of affordable health insurance plans, tailored to meet the needs of individuals and families across Texas. Whether you’re seeking individual coverage or a plan for your loved ones, navigating the insurance landscape can be a daunting task. This comprehensive guide will shed light on the intricacies of health insurance in Texas, empowering you to make informed decisions and secure the protection you deserve.

Individual Plans

For individuals not covered by employer-sponsored plans, individual health insurance plans emerge as a viable option. These plans are purchased directly from insurance companies, offering greater flexibility in terms of coverage and premiums compared to employer-sponsored plans. However, they can sometimes come with higher costs.

Types of Individual Plans

The Texas health insurance market offers a spectrum of individual plans, each designed to cater to specific needs and budgets. These plans typically fall into two categories:

-

Health Maintenance Organizations (HMOs): HMOs contract with a network of healthcare providers, limiting your choice of providers but often resulting in lower premiums.

-

Preferred Provider Organizations (PPOs): PPOs offer a more expansive network of providers, providing you with greater flexibility in choosing your healthcare professionals. However, this flexibility typically comes with higher premiums.

Factors to Consider When Choosing an Individual Plan

When selecting an individual health insurance plan, several crucial factors warrant your consideration:

-

Coverage: Determine the specific healthcare services and benefits you require. This includes coverage for preventive care, prescription drugs, and specialty services.

-

Premiums: Premiums are the monthly payments you make to maintain your insurance coverage. Carefully assess your budget and choose a plan with premiums you can comfortably afford.

-

Deductibles: Deductibles represent the amount you pay out-of-pocket before your insurance coverage begins. Higher deductibles typically result in lower premiums.

-

Provider Network: Consider the network of healthcare providers available under the plan. If you have specific healthcare providers you prefer, ensure they are included in the network.

-

Copays and Coinsurance: Copays are fixed amounts you pay for certain services, such as doctor’s visits. Coinsurance represents the percentage of the cost you are responsible for after you meet your deductible.

Family Plans

Family health insurance plans extend coverage to multiple family members, providing a comprehensive safety net for your loved ones. These plans can be more cost-effective compared to purchasing individual plans for each family member.

Types of Family Plans

Family health insurance plans in Texas come in various forms, accommodating different family structures and needs:

-

Employer-Sponsored Family Plans: If you have employer-sponsored health insurance, you may have the option to extend coverage to your spouse and children.

-

Individual Family Plans: These plans are purchased directly from insurance companies and provide coverage for you and your family members.

-

Children’s Health Insurance Program (CHIP): CHIP provides low-cost health insurance coverage to children from families with moderate incomes.

Factors to Consider When Choosing a Family Plan

Similar to individual plans, several key factors should guide your decision-making process when selecting a family health insurance plan:

-

Coverage: Evaluate the plan’s coverage for preventive care, prescription drugs, and other essential healthcare services for your family.

-

Premiums: Assess the total premiums for the entire family and ensure they fit within your financial constraints.

-

Deductibles: Consider the deductibles for the family plan and how they impact your out-of-pocket expenses.

-

Provider Network: Determine if the plan’s provider network includes your preferred healthcare providers.

-

Copays and Coinsurance: Review the copays and coinsurance associated with the plan to estimate your potential costs for healthcare services.

Conclusion

Securing affordable health insurance in Texas is paramount to safeguarding your health and financial well-being. Whether you opt for an individual or family plan, carefully consider the factors outlined in this guide. By navigating the insurance landscape with informed choices, you can empower yourself and your loved ones with the protection you deserve. Remember, health insurance is not merely a financial investment; it’s an investment in peace of mind, ensuring that you can access the healthcare you need when you need it most.

Affordable Health Insurance Plans in Texas

Navigating the healthcare landscape can be a daunting task, especially when it comes to finding affordable health insurance plans. Texas residents face a unique set of challenges due to the state’s large uninsured population and limited Medicaid expansion. However, there are a plethora of options available to help Texans get the coverage they need without breaking the bank.

Types of Health Insurance Plans

- Employer-Sponsored Insurance: For those fortunate enough to have an employer-sponsored plan, it’s typically the most affordable option. Employers often contribute a significant portion of the cost, making it a great value for employees.

- Individual Health Insurance: If you don’t have employer-sponsored insurance, you’ll need to purchase an individual plan on the open market. These plans can be more expensive, but can provide you with the flexibility and coverage you need.

- Government Programs: Government programs like Medicaid and CHIP provide health insurance to low-income individuals and families. These programs can be a lifeline for those who would otherwise be unable to afford health insurance.

- Short-Term Health Insurance: Short-term health insurance is a temporary option that can bridge the gap between jobs or provide coverage during a specific time period. These plans are typically less comprehensive than other options, but can be more affordable.

- Health Savings Accounts (HSAs): HSAs are tax-advantaged accounts that allow you to save money for future medical expenses. You can use HSA funds to pay for deductibles, copays, and other out-of-pocket expenses. HSAs can be paired with high-deductible health plans (HDHPs) to reduce overall healthcare costs.

Choosing the Right Plan

When choosing an affordable health insurance plan in Texas, it’s important to consider your individual needs and budget. Factors to consider include:

- Coverage: Determine what type of coverage you need, including doctor visits, hospital stays, prescriptions, and preventive care.

- Premiums: Monthly premiums are the amount you pay for your insurance. Consider both the premium amount and the out-of-pocket costs (deductibles, copays, etc.) when evaluating affordability.

- Deductibles: A deductible is the amount you pay out-of-pocket before your insurance starts to cover costs. Higher deductibles typically lower premiums, but can result in higher out-of-pocket expenses if you have significant medical needs.

- Network: Choose a plan with a network of doctors and hospitals that you prefer. In-network providers typically have lower costs than out-of-network providers.

- Customer Service: Look for plans with a reputation for good customer service and easy accessibility.

Affordable Health Insurance Plans in Texas

There are a number of affordable health insurance plans available in Texas. Here are a few options to consider:

- Ambetter from Superior HealthPlan: Ambetter offers a range of affordable plans with low premiums and deductibles.

- Blue Cross Blue Shield of Texas: BCBS offers a variety of plans, including HMOs, PPOs, and HDHPs.

- Cigna: Cigna provides a wide network of doctors and hospitals, as well as affordable plans for individuals and families.

- Humana: Humana offers a range of plans, including Medicare Advantage plans for seniors.

- UnitedHealthcare: UnitedHealthcare provides a nationwide network of doctors and hospitals, as well as a variety of affordable plans.

Getting affordable health insurance in Texas doesn’t have to be a hassle. By understanding your options and comparing plans, you can find a plan that meets your needs and budget. Don’t go uninsured – take the time to explore your options and make sure you’re protected.

Medicaid and CHIP

Medicaid and CHIP are government programs that provide health insurance to low-income individuals and families. These programs can be a good option if you qualify for them, as they offer comprehensive coverage at a low cost.

To qualify for Medicaid in Texas, you must meet certain income and citizenship requirements. CHIP is available to children and young adults up to age 19 who meet certain income and citizenship requirements.

If you think you may qualify for Medicaid or CHIP, you can apply online or by contacting your local Medicaid office.

Employer-Sponsored Insurance

Employer-sponsored insurance is typically the most affordable option for health insurance. This is because employers often contribute a significant portion of the cost of the premium.

If you have the option to get health insurance through your employer, it’s worth considering. Employer-sponsored plans offer a number of advantages, including:

- Lower premiums: Employers often contribute a significant portion of the cost of the premium, making employer-sponsored plans more affordable than individual plans.

- Guaranteed coverage: Employer-sponsored plans are guaranteed coverage, regardless of your health status. This means you won’t be denied coverage if you have a pre-existing condition.

- Access to a wider network of providers: Employer-sponsored plans typically have access to a wider network of doctors and hospitals than individual plans. This means you’ll have more choice when it comes to choosing a doctor or hospital.

Individual Health Insurance

If you don’t have the option to get health insurance through your employer, you’ll need to purchase an individual plan on the open market. Individual plans can be more expensive than employer-sponsored plans, but they can provide you with the flexibility and coverage you need.

When shopping for an individual health insurance plan, it’s important to compare plans carefully. Consider the following factors:

- Coverage: Determine what type of coverage you need, including doctor visits, hospital stays, prescriptions, and preventive care.

- Premiums: Monthly premiums are the amount you pay for your insurance. Consider both the premium amount and the out-of-pocket costs (deductibles, copays, etc.) when evaluating affordability.

- Deductibles: A deductible is the amount you pay out-of-pocket before your insurance starts to cover costs. Higher deductibles typically lower premiums, but can result in higher out-of-pocket expenses if you have significant medical needs.

- Network: Choose a plan with a network of doctors and hospitals that you prefer. In-network providers typically have lower costs than out-of-network providers.

- Customer Service: Look for plans with a reputation for good customer service and easy accessibility.

Short-Term Health Insurance

Short-term health insurance is a temporary option that can bridge the gap between jobs or provide coverage during a specific time period. These plans are typically less comprehensive than other options, but can be more affordable.

Short-term health insurance plans typically have lower premiums than traditional health insurance plans. However, they also have lower coverage limits and may not cover certain types of care, such as pre-existing conditions.

Short-term health insurance plans can be a good option if you need temporary coverage and are healthy. However, they are not a substitute for traditional health insurance.

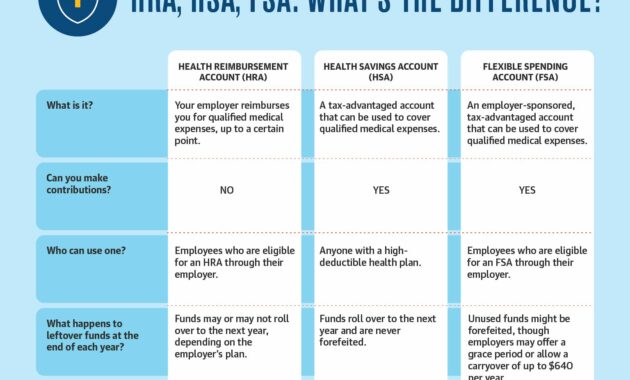

Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) are tax-advantaged accounts that allow you to save money for future medical expenses. You can use HSA funds to pay for deductibles, copays, and other out-of-pocket expenses.

HSAs can be paired with high-deductible health plans (HDHPs) to reduce overall healthcare costs. HDHPs have lower premiums than traditional health insurance plans, but higher deductibles.

If you have a high-deductible health plan, you can contribute up to $3,650 to your HSA in 2023 ($7,300 for family coverage). Withdrawals from your HSA are tax-free if they are used to pay for qualified medical expenses.

HSAs can be a great way to save money on healthcare costs. However, they are not right for everyone. You should consider your individual needs and financial situation before opening an HSA.

{kind=link}