Affordable Health Insurance Plans

In this day and age, healthcare costs are spiraling out of control, and many people are struggling to afford the coverage they need. If you’re one of the millions of Americans who are uninsured or underinsured, don’t despair. There are still affordable health insurance plans available, and we’ll help you find the right one for your needs.

One of the most important things to consider when choosing a health insurance plan is the premium. This is the monthly payment you’ll make to your insurance company. Premiums can vary widely, so it’s important to compare quotes from several different insurers before you make a decision.

Another important factor to consider is the deductible. This is the amount of money you’ll have to pay out-of-pocket before your insurance coverage kicks in. Deductibles can also vary widely, so it’s important to choose a plan with a deductible that you can afford.

Finally, you’ll want to consider the coverage limits. These limits determine how much your insurance company will pay for covered services. Coverage limits can vary widely, so it’s important to choose a plan with limits that are high enough to meet your needs.

If you’re not sure where to start your search for affordable health insurance, there are a few resources available to help you. You can contact your state’s health insurance marketplace, or you can use an online health insurance broker. These brokers can help you compare quotes from different insurers and find a plan that’s right for you.

What are the different types of affordable health insurance plans?

There are a few different types of affordable health insurance plans available, including:

- Health Maintenance Organizations (HMOs): HMOs are a type of managed care plan that offers comprehensive coverage at a lower cost. With an HMO, you’ll have to choose a primary care physician (PCP) who will coordinate your care. You’ll also need to get referrals from your PCP before you can see a specialist.

- Preferred Provider Organizations (PPOs): PPOs are another type of managed care plan that offers more flexibility than HMOs. With a PPO, you can choose any doctor or specialist you want, but you’ll pay a higher copay if you see a doctor who is not in your network.

- Exclusive Provider Organizations (EPOs): EPOs are a type of managed care plan that is similar to HMOs, but they offer even less flexibility. With an EPO, you can only see doctors and specialists who are in your network.

- Point-of-Service (POS) plans: POS plans are a type of managed care plan that offers a combination of HMO and PPO features. With a POS plan, you’ll have to choose a primary care physician (PCP), but you can also see specialists without a referral. You’ll pay a higher copay if you see a specialist who is not in your network.

How do I choose the right affordable health insurance plan for me?

When choosing an affordable health insurance plan, there are a few things you’ll need to consider, including:

- Your budget: How much can you afford to spend on health insurance each month?

- Your health needs: What kind of coverage do you need? Do you have any pre-existing conditions?

- Your lifestyle: How often do you see the doctor? Do you need coverage for prescription drugs?

Once you’ve considered these factors, you can start shopping for health insurance. Be sure to compare quotes from several different insurers before you make a decision.

Here are some tips for finding affordable health insurance:

- Shop around: Don’t just go with the first insurance company you find. Compare quotes from several different insurers to find the best deal.

- Consider a higher deductible: A higher deductible will lower your monthly premium. Just be sure to choose a deductible that you can afford.

- Look for discounts: Many insurers offer discounts for things like being a non-smoker or having a healthy lifestyle.

- Get help from a broker: If you’re not sure where to start, you can contact a health insurance broker. Brokers can help you compare quotes from different insurers and find a plan that’s right for you.

Health insurance is an important investment in your health and well-being. By following these tips, you can find an affordable health insurance plan that meets your needs.

What is Affordable Health Insurance?

Affordable health insurance is a plan that provides comprehensive medical coverage while keeping costs within reach. It’s a safety net that protects you from the financial burden of unexpected medical expenses, ensuring you can access the care you need without breaking the bank. Think of it as an umbrella that shields you from the storms of healthcare costs, keeping you financially secure and giving you peace of mind.

In today’s world, affordable health insurance is more crucial than ever. Medical expenses are on the rise, and without proper coverage, a single illness or accident could lead to financial ruin. It’s like driving a car without insurance—you’re taking a huge risk that could have devastating consequences.

Types of Affordable Health Insurance

There are various types of affordable health insurance plans available, each tailored to meet different needs and budgets. Let’s explore the most common options:

1. Health Maintenance Organizations (HMOs)

HMOs offer comprehensive coverage at a fixed monthly premium. You’ll have access to a network of doctors and hospitals, and you’ll typically pay less for copays and deductibles. The catch? You’re limited to using providers within the HMO’s network, which may restrict your choice of doctors.

2. Preferred Provider Organizations (PPOs)

PPOs provide more flexibility than HMOs. You can see any doctor you want, whether they’re in the PPO’s network or not. However, you’ll pay more for out-of-network care. PPOs offer a balance between affordability and choice, making them a popular option for many people.

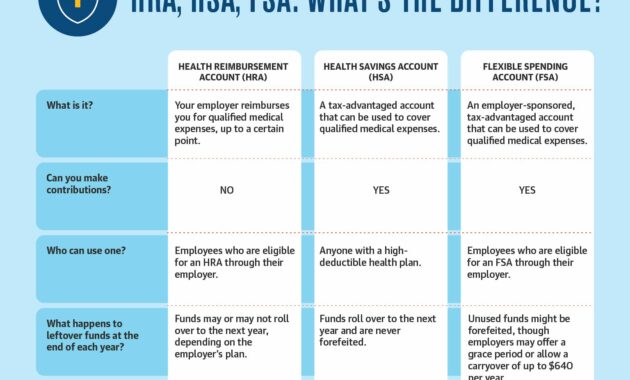

3. High-Deductible Health Plans (HDHPs)

HDHPs come with lower monthly premiums but higher deductibles. You’ll have to pay more out-of-pocket before your insurance kicks in. However, HDHPs often come with tax-advantaged savings accounts, such as Health Savings Accounts (HSAs), which can help you save for medical expenses.

4. Catastrophic Health Plans

Catastrophic health plans are designed for young and healthy individuals who are less likely to need frequent medical care. These plans have very low monthly premiums but extremely high deductibles. They’re meant to provide coverage for catastrophic events, such as major accidents or illnesses.

Choosing the Right Affordable Health Insurance Plan

Selecting the right affordable health insurance plan can be overwhelming. Here are some key factors to consider:

1. **Your health needs:** Consider your current and future health concerns. If you have chronic conditions or expect to need extensive medical care, you’ll need a plan with more comprehensive coverage.

2. **Your budget:** Determine how much you can afford to pay for monthly premiums, deductibles, and copays. Don’t overstretch your finances—choose a plan that fits your budget comfortably.

3. **Your lifestyle:** Consider your lifestyle and how it might impact your health insurance needs. If you’re active and adventurous, you may want a plan that covers accidents and injuries.

Affordable Health Insurance for Low-Income Individuals

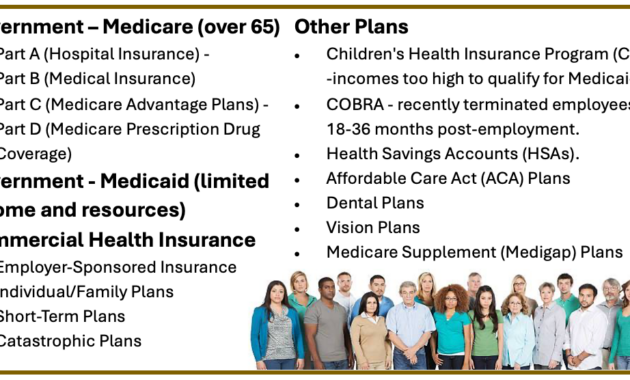

If you’re struggling financially, don’t despair. There are affordable health insurance options available to low-income individuals. Government programs like Medicaid and the Children’s Health Insurance Program (CHIP) provide coverage to those who qualify.

Additionally, some states have expanded Medicaid eligibility to cover more people. Check your state’s Medicaid website to see if you qualify. Don’t let your income be a barrier to accessing affordable health insurance.

Affordable Health Insurance: A Comprehensive Guide

Navigating the labyrinth of health insurance plans can be daunting, but it’s a crucial step towards securing your health and financial well-being. The good news is that there are plenty of affordable options out there, so you don’t have to break the bank to protect yourself and your loved ones.

Types of Affordable Health Insurance Plans

The world of health insurance plans can seem like a tangled web, but understanding the different types can help you make an informed decision. Here’s a breakdown of the most common affordable options:

Health Maintenance Organizations (HMOs)

HMOs are known for their low premiums and comprehensive coverage. You’ll have a primary care physician (PCP) who acts as your gatekeeper, referring you to specialists if necessary. The downside is that HMOs have more restrictions than other plans, and you may have to stay within a specific network of providers.

Preferred Provider Organizations (PPOs)

PPOs offer more flexibility than HMOs, allowing you to see doctors both inside and outside their network. However, you’ll typically pay more for out-of-network care. PPOs provide a good balance between cost and coverage, making them a popular choice for those who want some freedom in their provider choices.

Exclusive Provider Organizations (EPOs)

EPOs are similar to HMOs, but they offer even narrower networks of providers. In exchange for this limited choice, EPOs typically have lower premiums than HMOs. EPOs work best for those who have a preferred healthcare provider and don’t anticipate seeing specialists often.

High-Deductible Health Plans (HDHPs)

HDHPs have lower monthly premiums but higher deductibles. This means you’ll pay more out-of-pocket for medical expenses before your insurance kicks in. HDHPs are paired with Health Savings Accounts (HSAs), which allow you to save pre-tax dollars for healthcare costs. This can be a smart option for those who are healthy and don’t anticipate major medical expenses.

Other Affordable Options

In addition to the plans mentioned above, there are other affordable options available, such as:

- Medicaid: This government program provides health insurance to low-income individuals and families.

- CHIP: This program provides health insurance to children from low-income families.

- Medicare: This program provides health insurance to people over 65 and those with certain disabilities.

Factors to Consider When Choosing a Plan

When choosing an affordable health insurance plan, there are several factors to consider:

- Coverage: Make sure the plan covers the essential health benefits you need, including doctor visits, hospitalization, and prescription drugs.

- Premiums: The premiums are the monthly payments you’ll make to the insurance company. Consider your budget and choose a plan you can afford.

- Deductibles: The deductible is the amount you have to pay out-of-pocket before your insurance coverage kicks in. A higher deductible can lower your premiums, but it also means you’ll have to pay more for medical expenses.

- Copayments and coinsurance: These are the fixed amounts you pay for specific medical services, such as doctor visits or prescription drugs.

- Provider network: If you have a preferred healthcare provider, make sure they’re included in the plan’s network.

Tips for Finding Affordable Healthcare

Finding affordable health insurance doesn’t have to be a headache. Here are a few tips:

- Shop around: Compare plans from different insurance companies to find the best coverage and price for your needs.

- Take advantage of discounts: Many insurance companies offer discounts for things like being a non-smoker, getting a flu shot, or signing up for automatic payments.

- Consider a high-deductible plan: If you’re young and healthy, a high-deductible plan can save you money on premiums. Just make sure you have an HSA or other savings plan in place to cover potential medical expenses.

Conclusion

Affordable health insurance is within your reach. By understanding the different types of plans and considering the factors discussed in this article, you can find a policy that fits your needs and budget. So don’t wait, take action today to protect your health and financial well-being.

Affordable Health Insurance: A Lifeline in the Labyrinth of Medical Expenses

In the realm of healthcare, soaring medical costs can cast a long shadow over financial stability. The prospect of navigating this labyrinthine system without adequate health insurance can be daunting, but fear not! With careful planning and informed choices, an affordable health insurance plan can serve as a beacon of hope, illuminating the path toward financial well-being and peace of mind. Enter the realm of affordable health insurance, where premiums are manageable, coverage is comprehensive, and out-of-pocket costs won’t break the bank.

How to Choose an Affordable Health Insurance Plan

Selecting an affordable health insurance plan is akin to embarking on a treasure hunt, where the prize is financial security and the map is a thorough understanding of the available options. To guide you on this quest, let’s delve into the key factors to consider:

Coverage: The Umbrella That Keeps You Dry

Coverage is the foundation of any health insurance plan. It provides the safety net that protects you from the financial downpours of medical expenses. When evaluating coverage, ask yourself: Does the plan encompass the essential health benefits mandated by law? Does it include preventive care, such as annual checkups and screenings, that can help prevent costly illnesses down the road? A comprehensive plan ensures that you’re covered for a wide range of healthcare needs, from routine appointments to unexpected emergencies.

Premiums: The Price of Peace of Mind

Premiums are the regular payments you make to maintain your health insurance coverage. Think of them as the toll you pay to cross the bridge of financial security. The amount you pay will vary depending on factors such as your age, health status, and the coverage level you choose. It’s crucial to strike a balance between affordability and the level of coverage you need. A higher premium may provide more comprehensive coverage, but it’s essential to ensure that the cost doesn’t strain your budget.

Deductibles: The First Line of Defense

A deductible is the amount you pay out of pocket before your insurance coverage kicks in. It acts as a buffer against smaller medical expenses, allowing you to save on your monthly premiums. However, a higher deductible means lower premiums but also higher out-of-pocket costs for initial medical expenses. It’s a trade-off that requires careful consideration.

Out-of-Pocket Costs: The Hidden Expenses

Out-of-pocket costs are the expenses you pay directly, even after meeting your deductible. They include copayments for doctor’s visits, prescription drug costs, and coinsurance, which is a percentage of the cost of covered services. It’s essential to factor in these costs when evaluating the affordability of a health insurance plan. Unexpected out-of-pocket expenses can quickly derail your financial plans, so it’s wise to choose a plan that minimizes these costs.

Navigating the Affordable Care Act: A Lifeline for Those in Need

The Affordable Care Act (ACA) has been a game-changer in the world of health insurance. Enacted in 2010, the ACA has made health insurance more accessible and affordable for millions of Americans. One of the key provisions of the ACA is the establishment of health insurance marketplaces, where individuals and families can compare plans and purchase coverage that meets their needs and budget.

Subsidies: A Helping Hand for Those Who Qualify

The ACA also provides subsidies to help low- and moderate-income individuals and families afford health insurance. These subsidies can significantly reduce the cost of premiums, making health insurance more accessible to those who need it most. If you qualify for subsidies, they can be applied to your monthly premium payments, making health insurance a more manageable expense.

Medicaid Expansion: A Lifeline for the Most Vulnerable

Medicaid is a government-funded health insurance program for low-income individuals and families. The ACA expanded Medicaid eligibility to millions of Americans, providing them with access to affordable health care. If you meet the income requirements, Medicaid can provide comprehensive coverage with minimal out-of-pocket costs.

Employer-Sponsored Health Insurance: A Convenient Option for Many

For many Americans, employer-sponsored health insurance is the most common way to obtain coverage. Employer-sponsored plans offer several advantages, including convenience, payroll deductions, and potential cost savings. However, it’s important to carefully evaluate the coverage and costs of your employer-sponsored plan to ensure that it meets your needs and budget.

Group Rates: The Power of Collective Bargaining

Employer-sponsored plans often offer group rates, which can result in lower premiums for employees. By pooling together a large number of individuals, employers can negotiate more favorable terms with insurance companies, passing on the savings to their employees.

Payroll Deductions: A Convenient Way to Pay

Payroll deductions allow employees to pay their health insurance premiums directly from their paycheck. This convenient payment method helps ensure that premiums are paid on time, avoiding any potential lapses in coverage.

Employer Contributions: A Potential Cost-Saving Measure

Many employers contribute to their employees’ health insurance premiums, further reducing the cost of coverage for employees. Employer contributions vary widely, so it’s important to inquire about your employer’s contribution policy to determine the potential cost savings.

Individual Health Insurance Plans: Flexibility and Control for the Self-Employed

For the self-employed and those who don’t have access to employer-sponsored coverage, individual health insurance plans offer flexibility and control. Individual plans allow you to customize your coverage and choose a plan that meets your specific needs and budget.

Choice and Flexibility: Tailoring Coverage to Your Needs

With individual health insurance plans, you have the freedom to choose the coverage level, deductible, and out-of-pocket costs that best suit your needs and financial situation. You can also select from a wide range of plans offered by different insurance companies, ensuring that you find a plan that fits your unique circumstances.

Direct Relationship with the Insurance Company: Unmediated Communication

When you purchase an individual health insurance plan, you have a direct relationship with the insurance company. This eliminates the middleman, allowing for more transparent communication and streamlined resolution of any issues that may arise.

Potential Tax Deductions: A Financial Silver Lining

In some cases, premiums paid for individual health insurance plans may be eligible for tax deductions. This can further reduce the cost of coverage, making it more affordable. However, it’s important to consult with a tax professional to determine your eligibility for tax deductions.

Additional Tips for Finding an Affordable Health Insurance Plan

Beyond the key factors discussed above, here are some additional tips to help you find an affordable health insurance plan:

- Shop around: Compare plans from different insurance companies to find the best combination of coverage, premiums, and out-of-pocket costs.

- Consider a high-deductible plan with a health savings account (HSA): HSAs allow you to save money tax-free to cover qualified medical expenses, including your deductible.

- Look for plans with preventive care benefits: Preventive care can help you avoid costly health problems down the road, so look for plans that cover preventive services with no out-of-pocket costs.

- Take advantage of discounts: Some insurance companies offer discounts for healthy habits, such as non-smoking or participating in wellness programs.

- Consider catastrophic health insurance: Catastrophic health insurance plans have lower premiums but higher deductibles. They’re designed to cover major medical expenses in case of a catastrophic illness or injury.

Conclusion: Securing Your Health Without Breaking the Bank

Navigating the healthcare system can be a daunting task, but finding an affordable health insurance plan doesn’t have to be. By understanding the key factors involved, taking advantage of available resources, and following these tips, you can secure the coverage you need without breaking the bank. Remember, health insurance is not a luxury; it’s a lifeline that protects your financial well-being and gives you peace of mind knowing that you’re prepared for whatever life throws your way.

{kind=link}