Affordable Health Insurance Plans

In the realm of healthcare, where costs can soar to dizzying heights, safeguarding your well-being shouldn’t come at an exorbitant price. Enter affordable health insurance plans, the knight in shining armor that rescues you from financial distress while ensuring your access to essential medical services. Whether you’re navigating the complexities of the individual market or seeking coverage through your employer, this comprehensive guide will empower you to make informed decisions about your health insurance journey. Our mission is to unravel the intricacies of affordable health insurance, arming you with the knowledge to secure a plan that aligns with your budget and health needs.

Understanding Affordable Health Insurance

Before embarking on your search for affordable health insurance, it’s imperative to grasp the fundamentals that underpin these plans. Understanding the different types of coverage, premiums, deductibles, and copays will equip you to make discerning choices. Let’s delve into the inner workings of affordable health insurance, deciphering the jargon and empowering you to navigate the healthcare landscape with confidence.

Types of Health Insurance Plans

The world of health insurance encompasses a kaleidoscope of plans, each tailored to specific needs and circumstances. Navigating this labyrinth can be daunting, but fear not! We’ve distilled the complexities into digestible categories, providing you with a clear understanding of the options that lie before you: HMOs, PPOs, EPOs, and POS plans. HMOs, the gatekeepers of healthcare, restrict your access to a network of providers but reward you with lower premiums. PPOs, on the other hand, grant you the freedom to roam beyond the network, albeit at a slightly higher cost. EPOs, similar to HMOs, limit your provider choices within a specific network, while POS plans offer a hybrid approach, combining elements of both HMOs and PPOs. Understanding these distinctions is paramount in selecting a plan that harmonizes with your lifestyle and preferences.

In addition to understanding the different types of health insurance plans, it’s equally important to familiarize yourself with the terms that govern them. Premiums, deductibles, and copays – these aren’t just buzzwords; they’re the cornerstones of your plan’s financial structure. Premiums, the regular payments you make to maintain coverage, lay the foundation for your health insurance journey. Deductibles, the amounts you pay out-of-pocket before insurance kicks in, act as financial buffers. Copays, the fixed fees you pay for doctor’s visits or prescriptions, represent your direct contribution to specific medical services. Grasping these concepts will empower you to make informed decisions about your coverage and financial obligations.

Now that you’ve gained a solid understanding of the different types of health insurance plans and the key terms associated with them, it’s time to embark on the quest for affordable coverage. Let’s explore the strategies and resources that will guide you towards a plan that meets both your budgetary constraints and your health needs.

Affordable Health Insurance Plans: A Lifeline for the Financially Burdened

Securing affordable health insurance can be like navigating a labyrinth, leaving many individuals feeling lost and overwhelmed. However, with the right guidance, you can emerge from this maze with a plan that fits both your budget and your health needs.

How to Find Affordable Health Insurance Plans

Like a detective on the trail of a hidden treasure, there are several avenues you can explore to uncover affordable health insurance plans. Let’s embark on a journey of discovery:

Method 1: Comparing Plans from Different Insurers

Just as a chef carefully selects ingredients to create a tantalizing dish, you’ll want to meticulously compare plans from different insurers to find the perfect fit. Scour the market, gather information, and don’t settle for the first option that comes your way. Evaluate deductibles, co-pays, and coverage limits with the precision of a surgeon.

But wait, there’s more! Don’t forget to check the insurer’s financial stability. After all, you wouldn’t want to put your health in the hands of a company that could vanish like a wisp of smoke. Look for insurers with strong ratings from reputable agencies like AM Best or Standard & Poor’s.

Method 2: Negotiating with Your Employer

If you’re lucky enough to have an employer who offers health insurance, don’t let this golden opportunity slip through your fingers. Engage in the art of negotiation like a seasoned diplomat. Explore your options, ask questions, and don’t be afraid to put your bargaining chips on the table.

Remember, knowledge is power. Research typical premiums and benefits for your industry and location. This ammunition will strengthen your position during negotiations. And hey, don’t be shy about asking for a higher contribution from your employer. It’s worth a shot, right?

Method 3: Getting Help from a Broker

Navigating the health insurance maze can be daunting, especially if you’re not a seasoned adventurer. That’s where a broker can come to your rescue, like a beacon of light in the darkest of nights. These savvy professionals have an in-depth understanding of the market and can guide you through the complexities of choosing a plan.

So, how do you find a reputable broker? Tap into your network, ask for recommendations, and read online reviews. Once you’ve found a few candidates, interview them like you’re hiring a personal assistant. After all, you’re entrusting them with your health and finances.

Method 4: Exploring Government Subsidies

If your income falls within certain limits, you may qualify for government subsidies that can significantly reduce your health insurance costs. These subsidies are like a financial lifeline, helping you bridge the gap between what you can afford and the cost of coverage.

To determine your eligibility, visit the Health Insurance Marketplace website. It’s like having a personal financial advisor at your fingertips, providing you with tailored information and guidance.

Method 5: Considering High-Deductible Health Plans (HDHPs)

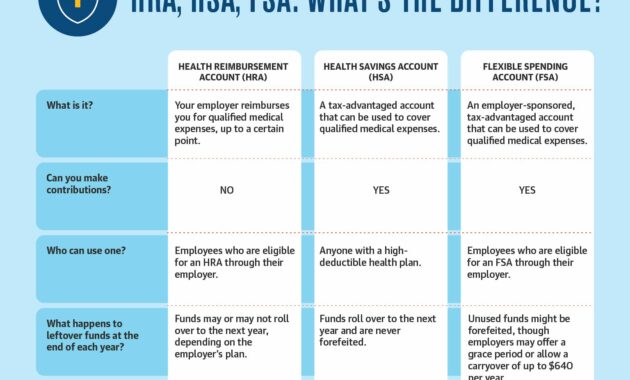

If you’re in good health and rarely use medical services, a high-deductible health plan (HDHP) could be a cost-effective option. These plans typically have lower monthly premiums but higher deductibles. However, they often come with a health savings account (HSA), which allows you to save money tax-free to cover medical expenses.

Think of an HDHP as a financial puzzle. You’ll pay less each month, but you’ll need to have some savings set aside to cover medical costs before the insurance kicks in. It’s like having a rainy day fund for your health.

The Bottom Line

Finding affordable health insurance doesn’t have to be a daunting task. By following these proven strategies, you can uncover a plan that meets your budget and health needs. Remember, it’s an investment in your well-being, and it’s worth spending the time to find the right fit.

So, embark on this journey with a positive mindset and a determination to find affordable health coverage. Your health and your wallet will thank you.

Affordable Health Insurance Plans: Everything You Need to Know

In today’s unpredictable healthcare landscape, finding affordable health insurance can feel like navigating a labyrinth. From skyrocketing premiums to confusing jargon, the process can leave even the most informed consumers feeling overwhelmed. That’s why we’ve compiled this comprehensive guide to help you decipher the complexities of health insurance and find a plan that fits your budget and health needs.

Before diving into the specifics, let’s address the elephant in the room: what constitutes an “affordable” health insurance plan? The definition varies depending on your income and circumstances, but generally speaking, an affordable plan should cost around 10% or less of your annual income.

Types of Affordable Health Insurance Plans

When it comes to affordable health insurance plans, there are a few different options to choose from. Each type has its own unique set of benefits and drawbacks, so it’s crucial to compare plans before making a decision.

1. Health Maintenance Organizations (HMOs)

HMOs are known for their low monthly premiums and extensive coverage. However, they also come with some restrictions. With an HMO, you’ll need to choose a primary care physician (PCP) who will coordinate your care. You’ll also need to get referrals from your PCP to see specialists or receive certain services.

2. Preferred Provider Organizations (PPOs)

PPOs offer more flexibility than HMOs, but they come with higher premiums. With a PPO, you can choose any doctor or specialist you want, without the need for referrals. You’ll also have access to a broader network of healthcare providers.

3. Exclusive Provider Organizations (EPOs)

EPOs are similar to HMOs in that you’ll need to choose a primary care physician and get referrals for specialist care. However, EPOs typically have lower premiums than HMOs. Additionally, EPOs often offer a wider range of doctors to choose from within their network compared to HMOs, but it is still more limited than PPOs.

Choosing the right type of health insurance plan depends on your individual needs and budget. If you’re looking for a low-cost option with limited flexibility, an HMO might be a good choice. If you value flexibility and access to a wide range of providers, a PPO might be a better fit. And if you’re on a tight budget and willing to trade flexibility for lower premiums, an EPO could be worth considering.

Beyond these three main types of health insurance plans, there are a few other options to explore, including:

- High-deductible health plans (HDHPs): These plans have lower monthly premiums but higher deductibles. This means you’ll pay more out of pocket for medical expenses until you meet your deductible.

- Health savings accounts (HSAs): These accounts allow you to save money tax-free for medical expenses. HSAs can be paired with HDHPs to further reduce your healthcare costs.

- Short-term health insurance: These plans are a good option for people who need temporary coverage, such as between jobs or during a transition period.

Factors to Consider When Choosing a Plan

When comparing affordable health insurance plans, there are a number of factors to consider, including:

1. Monthly premiums: This is the amount you’ll pay each month for your health insurance coverage.

2. Deductibles: This is the amount you’ll need to pay out of pocket for medical expenses before your insurance starts to cover them.

3. Copayments: These are fixed amounts you’ll pay for certain medical services, such as doctor’s visits or prescription drugs.

4. Coinsurance: This is the percentage of the cost of medical services that you’ll pay after you’ve met your deductible.

5. Out-of-pocket maximum: This is the most you’ll have to pay for medical expenses in a year.

6. Network of providers: This is the group of doctors, hospitals, and other healthcare providers that your insurance plan covers.

7. Prescription drug coverage: This is the coverage your plan provides for prescription medications.

It’s important to choose a plan that fits your budget and health needs. If you’re healthy and don’t have any major medical conditions, a plan with a high deductible and low monthly premiums might be a good option. If you have a chronic condition or expect to have high medical expenses, a plan with a lower deductible and higher monthly premiums might be a better choice.

Where to Find Affordable Health Insurance Plans

There are a few different ways to find affordable health insurance plans. You can:

- Contact a health insurance broker: A broker can help you compare plans and find the best option for your needs.

- Shop for plans online: There are a number of websites where you can compare health insurance plans and get quotes.

- Check with your employer: Many employers offer health insurance plans to their employees.

- Get coverage through a government program: There are a number of government programs that provide health insurance coverage to low-income individuals and families.

Finding affordable health insurance doesn’t have to be a daunting task. By understanding the different types of plans available and considering your individual needs, you can find a plan that fits your budget and provides the coverage you need.

Affordable Health Insurance Plans: Your Key to a Healthier, More Secure Future

In the current healthcare landscape, securing affordable health insurance is no longer a luxury but a necessity. With the rising cost of medical care, the absence of adequate coverage can lead to financial ruin. Affordable health insurance plans offer a lifeline, providing individuals and families with peace of mind, financial protection, and access to vital healthcare services.

Benefits of Affordable Health Insurance Plans

The benefits of having affordable health insurance extend far beyond mere financial security. It empowers individuals to take control of their health, empowering them to seek preventive care, manage chronic conditions, and respond effectively to unforeseen medical emergencies.

- Peace of Mind: Affordable health insurance alleviates the anxiety associated with unexpected medical expenses. Knowing that you have coverage in place provides peace of mind, allowing you to focus on your health and well-being without the burden of financial worries.

- Financial Protection: Medical expenses can be staggering, often amounting to thousands of dollars. Without adequate insurance, you may be forced to pay these expenses out-of-pocket, potentially leading to financial hardship or even bankruptcy. Affordable health insurance plans act as a safety net, shielding you from the financial devastation associated with major medical events.

- Access to Quality Medical Care: Affordable health insurance plans provide access to a broad range of medical services, including preventive care, primary care, specialist visits, hospitalization, and prescription drugs. This comprehensive coverage ensures that you have the resources you need to maintain good health and address any medical issues that may arise.

Understanding Affordable Health Insurance Plans

The landscape of affordable health insurance plans can be complex and overwhelming, but understanding the key components can help you make informed decisions.

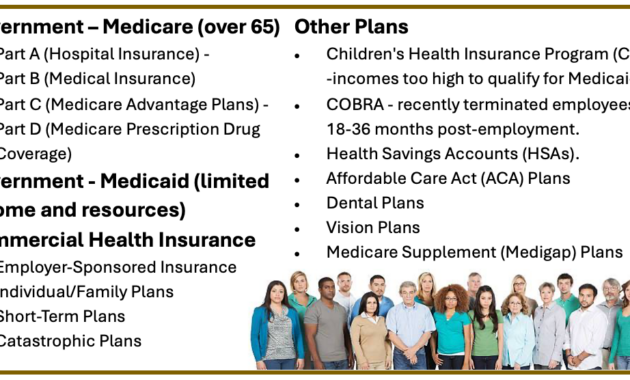

- Types of Plans: There are various types of health insurance plans available, including Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and High-Deductible Health Plans (HDHPs). Each type offers a unique combination of benefits, costs, and provider networks.

- Premiums and Deductibles: Premiums are the monthly payments you make to maintain your insurance coverage. Deductibles are the amount you pay out-of-pocket before your insurance begins to cover expenses.

- Copays and Coinsurance: Copays are fixed amounts you pay for specific medical services, such as visiting a doctor or filling a prescription. Coinsurance is a percentage of the cost of medical services that you are responsible for paying after meeting your deductible.

Finding Affordable Health Insurance Plans

Navigating the healthcare marketplace to find affordable health insurance plans can be a daunting task. Here are some strategies to help you get started.

- Research and Compare: Take the time to research different health insurance plans and compare their benefits, costs, and provider networks. Online tools and insurance brokers can help you gather information and identify plans that meet your specific needs.

- Consider Your Budget: Determine how much you can afford to spend on health insurance premiums and out-of-pocket expenses. This will help you narrow your search to plans that fit your financial constraints.

- Explore Government Programs: Government programs, such as Medicaid and Medicare, provide affordable health insurance options for low-income individuals and seniors.

Securing affordable health insurance is an essential step toward achieving a healthier, more secure future. By understanding the benefits, types, and strategies for finding affordable plans, you can empower yourself to make informed decisions and protect your well-being.

{kind=link}