Affordable Health Insurance Plans: A Comprehensive Guide to Finding the Right Coverage

In today’s world, health insurance is no longer a luxury but a necessity. The cost of medical care is skyrocketing, and without adequate coverage, a single illness or accident can financially cripple you. Fortunately, there are a variety of affordable health insurance plans available to fit every budget and need. In this article, we’ll take a deep dive into the world of health insurance, exploring different types of plans and providing tips on how to find the best coverage for you.

Understanding Health Insurance Plans

Health insurance is a contract between you and an insurance company. In exchange for paying a monthly premium, the insurance company agrees to cover a portion of your medical expenses. There are a variety of different health insurance plans available, each with its own unique set of benefits and drawbacks. The three most common types of plans are HMOs, PPOs, and EPOs.

Different Types of Health Insurance Plans

HMOs (Health Maintenance Organizations)

HMOs are a type of health insurance plan that emphasizes preventive care. In order to keep costs down, HMOs typically require you to choose a primary care physician (PCP) who will oversee your care. Your PCP will refer you to specialists as needed, and you will only be able to see out-of-network providers in emergency situations.

Advantages of HMOs:

- Lower monthly premiums

- No deductibles or copays for preventive care

- Access to a wide network of providers

Disadvantages of HMOs:

- Limited choice of providers

- May require referrals to see specialists

- May not cover out-of-network care

PPOs (Preferred Provider Organizations)

PPOs are a type of health insurance plan that offers more flexibility than HMOs. With a PPO, you can choose any doctor or hospital you want, both in and out of network. However, you will pay a higher premium for the increased flexibility.

Advantages of PPOs:

- Greater choice of providers

- No referrals required to see specialists

- Coverage for out-of-network care

Disadvantages of PPOs:

- Higher monthly premiums

- Deductibles and copays for all services

- Limited coverage for out-of-network care

EPOs (Exclusive Provider Organizations)

EPOs are a type of health insurance plan that is similar to HMOs in many ways. The main difference is that EPOs do not cover out-of-network care. This means that you will need to choose a provider within the EPO’s network, or you will have to pay for the entire cost of your care out of pocket.

Advantages of EPOs:

- Lower monthly premiums

- No deductibles or copays for preventive care

- Access to a wide network of providers

Disadvantages of EPOs:

- Limited choice of providers

- May require referrals to see specialists

- No coverage for out-of-network care

Now that you have a basic understanding of the different types of health insurance plans available, you can start shopping for a plan that meets your needs and budget. Here are a few tips to get you started:

- Compare quotes from multiple insurance companies. The cost of health insurance can vary significantly from one company to another, so it’s important to compare quotes before you make a decision.

- Consider your health needs. If you have a chronic condition or you’re planning to have a baby, you’ll need to make sure that your health insurance plan covers the services you need.

- Choose a plan that fits your budget. Health insurance can be expensive, so it’s important to choose a plan that you can afford.

Finding the right health insurance plan can be a daunting task, but it’s an important one. By taking the time to understand your options and compare quotes, you can find a plan that meets your needs and budget. And remember, if you have any questions, don’t hesitate to reach out to an insurance agent for help.

Affordable Health Insurance Plans: A Comprehensive Guide

Navigating the complex world of health insurance can be a daunting task, especially when affordability is a top priority. Fortunately, there are a plethora of affordable health insurance plans available to meet your needs. This comprehensive guide will delve into various factors that influence premiums, decoding the ins and outs of selecting the right plan for your wallet and well-being.

Factors Affecting Premiums

Premiums, or the monthly payments you make for health insurance, are not set in stone. They fluctuate based on several key factors, including:

Age

As we age, our bodies become more susceptible to health conditions, making us higher-risk individuals from an insurance company’s perspective. This increased risk translates into higher premiums for older adults compared to their younger counterparts.

Health History

Your health history plays a significant role in determining your premiums. Pre-existing conditions, chronic illnesses, and high-risk behaviors, such as smoking, can raise your premiums. This is because insurance companies view these factors as indicators of potential healthcare expenses.

Geographical Location

Believe it or not, where you live has a direct impact on your health insurance premiums. Healthcare costs vary widely across the country, and insurance companies adjust premiums accordingly. Metropolitan areas tend to have higher medical expenses, leading to higher premiums, while rural areas often benefit from lower healthcare costs and, subsequently, lower premiums.

Other Factors

In addition to the big three – age, health history, and geographical location – other factors can also affect your premiums, such as:

- Type of plan (HMO, PPO, EPO, etc.)

- Deductible

- Co-pays and co-insurance

- Dependent coverage

- Wellness programs and incentives

Health Insurance Plans – Affordable and Accessible

In today’s healthcare landscape, finding affordable health insurance plans can feel like a daunting task. But don’t fret! We’ve scoured the market to bring you a comprehensive guide to help you navigate the complexities of health insurance and discover plans that meet your budget and needs.

Finding Affordable Plans

Embarking on the journey to find affordable health insurance plans is not for the faint of heart. Luckily, you have options:

-

Employer-Sponsored Plans: If you’re fortunate enough to have an employer who offers health insurance, take advantage of it! These plans often come with lower premiums and out-of-pocket costs than individual plans.

-

Government Programs: Government programs like Medicaid and Medicare offer health insurance to low-income individuals and families, as well as seniors and people with disabilities. Eligibility varies based on income and assets, so check if you qualify.

-

Online Marketplaces: Online marketplaces, also known as health insurance exchanges, allow you to compare and purchase health insurance plans from multiple insurers. These marketplaces offer subsidies to help lower monthly premiums for those who qualify.

-

Shopping Around: Don’t just settle for the first plan you find. Take the time to compare plans from different insurers and brokers. Consider factors like monthly premiums, deductibles, co-pays, and out-of-pocket maximums. Remember, the cheapest plan isn’t always the best value.

Understanding Health Insurance Terms

Navigating the world of health insurance can be like deciphering a foreign language. Here are some key terms to help you find your way:

-

Premium: The monthly or annual fee you pay for your health insurance coverage.

-

Deductible: The amount you have to pay out-of-pocket before your insurance starts covering costs.

-

Co-pay: A fixed amount you pay for certain medical services, like doctor’s visits or prescriptions.

-

Out-of-Pocket Maximum: The maximum amount you have to pay for covered services in a year.

-

Network: A group of doctors, hospitals, and other healthcare providers that have agreed to provide services at discounted rates to insurance members.

Additional Tips for Saving Money

Finding affordable health insurance plans is a marathon, not a sprint. Here are a few more tips to help you save money on your coverage:

-

Choose a higher deductible: A higher deductible means lower monthly premiums. Just make sure you have enough savings to cover any unexpected medical expenses.

-

Use in-network providers: Staying within your insurance network can save you significant money on co-pays and other out-of-pocket costs.

-

Take advantage of preventive care: Most health insurance plans cover preventive care services, like checkups and screenings, at no cost to you. Take advantage of these services to stay healthy and avoid costly medical problems down the road.

-

Consider a health savings account (HSA): HSAs allow you to save money for qualified medical expenses on a pre-tax basis. This can reduce your overall healthcare costs and provide tax savings.

-

Negotiate with your provider: If you have a high deductible plan, don’t be afraid to negotiate with your doctor or hospital for lower rates on services. Just be prepared to pay upfront.

Conclusion

Finding affordable health insurance plans can be challenging, but it’s not impossible. By taking the time to understand your options, compare plans, and follow these tips, you can find coverage that fits your budget and provides you with peace of mind. Remember, having health insurance is like having a safety net. It’s there for you when you need it most, so make sure you have a plan in place to protect yourself and your loved ones.

Affordable Health Insurance Plans: A Guide for Every Budget

Navigating the healthcare maze can be daunting, especially when trying to find affordable health insurance plans. The medical field is often seen as a labyrinth, leaving many individuals feeling lost and overwhelmed. But fear not, dear reader! This comprehensive guide will illuminate your path towards finding the perfect plan to safeguard your health and finances.

Let’s dive right into the factors that influence the cost of health insurance: age, location, and the type of plan you choose. Age plays a significant role, with premiums typically rising as you get older. Location also matters, as healthcare costs vary from state to state. And lastly, the type of plan you select can impact your monthly expenses. As we delve into the various insurance options available, we’ll uncover the intricacies and benefits of each.

Government programs like Medicaid and Medicare offer a lifeline to low-income individuals and families. These programs provide essential health coverage, ensuring that financial constraints don’t stand in the way of accessing quality healthcare. For those who don’t qualify for government assistance, employer-sponsored plans are often a viable option. Many companies offer group health insurance plans, which typically come with lower premiums than individual plans.

If you find yourself without employer-sponsored insurance, the Health Insurance Marketplace is your go-to destination. This online platform allows you to shop for and compare plans from various insurance providers. The Marketplace also offers subsidies to help make coverage more affordable for those who qualify.

Now, let’s take a closer look at the different types of health insurance plans available: HMOs, PPOs, and EPOs. Each plan has its own unique structure and benefits. HMOs (Health Maintenance Organizations) provide coverage within a network of healthcare providers, offering lower premiums but potentially limiting your choice of doctors. PPOs (Preferred Provider Organizations) offer more flexibility, allowing you to see doctors outside of the network, but at a higher cost. EPOs (Exclusive Provider Organizations) are similar to HMOs, but with even more restrictions on the network of providers.

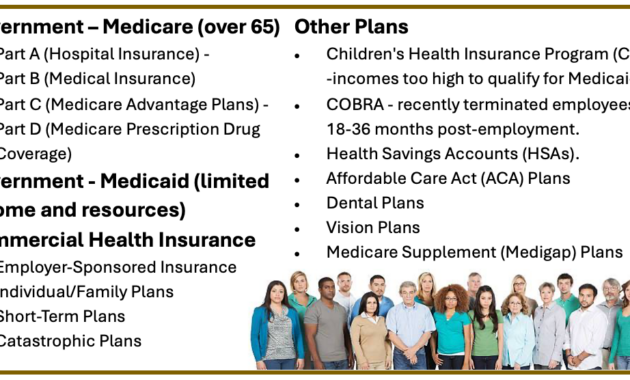

Government Assistance Programs

Government programs, such as Medicaid and Medicare, can provide health insurance coverage for low-income individuals and families. These programs are designed to ensure that everyone has access to affordable healthcare, regardless of their income.

**Medicaid** is a joint federal-state program that provides health coverage to low-income adults, children, pregnant women, and people with disabilities. Medicaid is administered by each state, so eligibility and benefits may vary. To qualify for Medicaid, you must meet certain income and resource requirements. In some states, Medicaid is also available to undocumented immigrants.

**Medicare** is a federal health insurance program for people aged 65 and older, as well as certain younger people with disabilities. Medicare has four parts: Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage). To qualify for Medicare, you must be a U.S. citizen or permanent resident and meet certain other requirements.

Employer-Sponsored Plans

Employer-sponsored health insurance plans are offered by many companies as a benefit to their employees. These plans typically offer lower premiums than individual plans because the employer pays a portion of the cost. To be eligible for an employer-sponsored plan, you must be an employee of the company.

Employer-sponsored plans can vary in terms of coverage and benefits. Some plans may have a wider network of providers than others. Some plans may also offer additional benefits, such as dental and vision coverage. It’s important to carefully review the details of your employer’s health insurance plan before enrolling.

Health Insurance Marketplace

The Health Insurance Marketplace is a government-run website where you can shop for and compare health insurance plans from different insurance companies. The Marketplace is available in every state. To be eligible for the Marketplace, you must not have access to affordable health insurance through your employer or a government program.

When you shop for health insurance on the Marketplace, you can compare plans based on their coverage, benefits, and cost. You can also see if you qualify for subsidies to help lower the cost of your premiums. If you qualify for subsidies, you will need to provide proof of income.

Types of Health Insurance Plans

There are three main types of health insurance plans: HMOs, PPOs, and EPOs. Each type of plan has its own unique structure and benefits.

**HMOs (Health Maintenance Organizations)** are a type of health insurance plan that provides coverage within a network of healthcare providers. HMOs typically have lower premiums than other types of plans. However, you may have to see a primary care doctor before you can see a specialist. HMOs are generally a good choice for people who don’t mind seeing doctors within a network. **PPOs (Preferred Provider Organizations)** are a type of health insurance plan that allows you to see doctors both within and outside of a network of healthcare providers. PPOs typically have higher premiums than HMOs, but they offer more flexibility. You can see any doctor you want, but you will pay more if you see a doctor outside of the network. PPOs are a good choice for people who want the flexibility to see doctors outside of a network.

EPOs (Exclusive Provider Organizations) are a type of health insurance plan that is similar to an HMO. EPOs have a network of healthcare providers, and you must see a doctor within the network to get coverage. EPOs typically have lower premiums than PPOs, but they offer less flexibility. You can only see doctors within the network, and you will have to pay more if you see a doctor outside of the network. EPOs are a good choice for people who want lower premiums and don’t mind seeing doctors within a network.

Health Insurance Plans: Affordable Options for Every Budget

Navigating the labyrinth of health insurance plans can be a daunting task, but it doesn’t have to be. With careful research and a keen eye for affordability, you can find a plan that fits your budget and provides the coverage you need. Whether you’re employed, self-employed, or seeking coverage for your family, there are countless options available. Let’s dive into the world of health insurance and explore the affordable plans that will keep you healthy and secure.

Employer-Sponsored Plans

If you’re fortunate enough to have an employer who offers health insurance, you’re in luck. Employer-sponsored plans often provide competitive rates and convenient access to healthcare. Your employer may cover a portion of the premiums, making the plan even more affordable. These plans typically offer a range of options, from basic coverage to comprehensive benefits. Discuss your needs with your employer to determine the best plan for you.

Individual and Family Plans

For those not covered by an employer-sponsored plan, individual and family plans offer flexibility and customization. You can choose from various plans and carriers to find one that meets your specific needs and budget. The premiums for these plans can vary depending on factors such as age, health status, and location. You may qualify for subsidies or tax credits to help offset the cost of coverage.

Health Maintenance Organizations (HMOs)

HMOs are a type of managed care plan that offers affordable premiums and a wide network of healthcare providers. HMOs typically require you to choose a primary care physician (PCP) who will coordinate your care and refer you to specialists as needed. This can provide a more streamlined and cost-effective healthcare experience.

Preferred Provider Organizations (PPOs)

PPOs are another type of managed care plan that offers more flexibility than HMOs. With a PPO, you can choose any provider within the network, including specialists, without a referral. While the premiums may be slightly higher than HMOs, PPOs provide greater freedom and choice.

High-Deductible Health Plans (HDHPs)

HDHPs are a type of health insurance plan that has a higher deductible but lower monthly premiums. This means you’ll pay more out-of-pocket for healthcare expenses before your insurance coverage kicks in. However, the lower premiums can save you money in the long run, especially if you’re generally healthy and don’t anticipate needing extensive medical care.

Supplemental Health Insurance

Supplemental health insurance policies can provide additional coverage to fill in the gaps of your primary plan. For example, you may purchase a dental or vision plan to cover expenses not covered by your main health insurance. Supplemental policies can also provide coverage for specific conditions, such as cancer or critical illnesses. These policies can provide peace of mind and enhance your overall health security.

Conclusion

Finding affordable health insurance doesn’t have to be a financial burden. By exploring the various options available, you can find a plan that fits your budget and provides the coverage you need. Whether you choose an employer-sponsored plan, an individual or family plan, or a supplemental policy, there’s a solution that will keep you and your loved ones healthy and protected. Take the time to research and compare plans to ensure you make the best decision for your specific needs.

Health Insurance Plans Affordable

Let’s face it, finding affordable health insurance plans can be a real pain in the neck. With so many options out there, it’s like trying to find a needle in a haystack. But fear not, fellow health-seekers! We’ve got your back. In this comprehensive guide, we’ll break down everything you need to know about finding and comparing health insurance plans that fit your budget and keep your wallet happy. So, grab a cup of coffee, get comfy, and let’s dive right in!

Understanding Health Insurance Basics

Before we start shopping for plans, let’s get a quick rundown of the basics. Health insurance is like a safety net that protects you from unexpected medical expenses. It’s like having a superhero sidekick that swoops in to save the day when you get sick or injured. Plans typically cover a range of services, from doctor visits to hospital stays, and even mental health care.

Types of Health Insurance Plans

There are various types of health insurance plans available, each with its own perks and quirks. Let’s explore some of the most common ones:

Health Maintenance Organizations (HMOs)

HMOs are like exclusive clubs where you have a primary care physician (PCP) who acts as your gatekeeper. You need a referral from your PCP to see specialists, but HMOs often offer lower premiums and out-of-pocket costs.

Preferred Provider Organizations (PPOs)

PPOs give you more flexibility by allowing you to see specialists without a referral. However, this convenience comes with higher premiums compared to HMOs.

Exclusive Provider Organizations (EPOs)

EPOs are similar to HMOs, but they have a narrower network of providers. This means you have a smaller selection of doctors and hospitals to choose from, but you may get lower premiums.

Point-of-Service (POS) Plans

POS plans combine features of HMOs and PPOs. You have a primary care physician like in an HMO, but you can still see specialists without a referral. However, out-of-network care is more expensive than in-network care.

Online Marketplaces

Online marketplaces, such as the Health Insurance Marketplace, allow individuals and families to compare and purchase health insurance plans from various providers. These marketplaces make it easy to find plans that meet your needs and budget. You can filter your search by factors like coverage, premiums, and deductibles. Plus, you may qualify for subsidies or tax credits to help lower your costs.

Brokers and Agents

Brokers and agents are licensed professionals who can help you find and enroll in health insurance plans. They can provide personalized advice and guide you through the enrollment process. However, they may charge a fee for their services.

Direct Enrollment

You can also enroll in health insurance plans directly through the insurance company’s website or by calling their customer service line. This option is often the most cost-effective, but it may require you to do more research to find the right plan for you.

Tips for Finding Affordable Health Insurance

Now that you know the basics, let’s get down to the nitty-gritty of finding affordable health insurance plans:

Consider a High-Deductible Health Plan (HDHP)

HDHPs have lower premiums but higher deductibles. This means you pay more out-of-pocket costs before your insurance starts covering expenses. However, HDHPs often come with a Health Savings Account (HSA), which allows you to save money tax-free for future medical expenses.

Look for Plans with Low Monthly Premiums

Monthly premiums are the fixed amount you pay each month for your health insurance. By choosing a plan with lower premiums, you can reduce your monthly expenses. However, keep in mind that plans with low premiums may have higher deductibles or out-of-pocket costs.

Maximize Your Out-of-Pocket Costs

Out-of-pocket costs are the expenses you pay before your insurance starts covering care. These costs include deductibles, copays, and coinsurance. By choosing a plan with lower out-of-pocket costs, you can minimize your financial burden when you need medical care.

Compare Plans from Different Providers

Don’t put all your eggs in one basket! Comparison shop from multiple insurance providers to find the best deals. Use online marketplaces or consult with brokers or agents to get quotes from different companies.

Take Advantage of Subsidies and Tax Credits

The government offers subsidies and tax credits to help low- and moderate-income individuals and families afford health insurance. Check if you qualify for these financial assistance programs to lower your costs.

Consider Catastrophic Health Insurance

Catastrophic health insurance is a bare-bones plan designed for healthy individuals who rarely seek medical care. It has low premiums but very high deductibles. This option may be suitable for young and healthy people who want to save money on premiums.

Negotiate with Your Employer

If you get health insurance through your employer, don’t be afraid to negotiate. Ask if there are any discounts or incentives available for employees who choose certain plans or meet specific wellness goals.

Conclusion

Finding affordable health insurance plans may seem like a daunting task, but it doesn’t have to be. By following these tips and utilizing the resources available, you can find a plan that fits your needs and budget. Remember, health insurance is an important investment in your well-being and financial security. So, take the time to research, compare, and choose a plan that gives you peace of mind and keeps your wallet happy.

Affordable Health Insurance Plans: A Lifeline for Financial Well-being

In an era where healthcare costs continue to skyrocket, finding affordable health insurance plans has become paramount. These plans serve as a financial lifeline, protecting individuals and families from the crippling costs of medical emergencies and unforeseen illnesses. With the right coverage, you can enjoy peace of mind knowing that your health and financial security are in good hands.

Navigating the complex world of health insurance can be daunting, but with the right information and guidance, you can find a plan that fits your needs and budget. This comprehensive guide will provide you with valuable tips and insights to help you secure affordable health insurance that doesn’t break the bank.

Understanding Health Insurance Terminology

Before we delve into the specifics of affordable health insurance plans, let’s first clarify some key terms:

- Premium: This is the monthly or yearly payment you make to your insurance company in exchange for coverage.

- Deductible: This is the amount you pay out-of-pocket before your insurance starts to cover costs.

- Coinsurance: This is the percentage of medical expenses you pay after meeting your deductible.

- Copayment: This is a fixed amount you pay for specific medical services, such as doctor’s visits or prescriptions.

- Out-of-pocket maximum: This is the maximum amount you pay for covered medical expenses in a year, after which your insurance covers 100% of costs.

Finding Affordable Health Insurance Plans

Now that we’ve covered the basics, let’s explore some strategies for finding affordable health insurance plans:

- Shop around: Don’t settle for the first plan you come across. Compare quotes from multiple insurance companies to find the best coverage at the lowest cost.

- Consider a high-deductible plan: Plans with higher deductibles typically have lower premiums. Just make sure you have enough savings to cover potential out-of-pocket costs in case of a medical emergency.

- Look for generic medications: Generic medications are just as effective as brand-name drugs, but they cost significantly less. Opting for generics can save you a bundle on prescription costs.

- Take advantage of employer-sponsored plans: If your employer offers health insurance, it’s often the most affordable option. The premiums may be subsidized by your employer, leading to substantial savings.

- Consider Medicaid or Medicare: Medicaid is a government program that provides health coverage to low-income individuals and families. Medicare is a government program that provides health coverage to people aged 65 and older or with certain disabilities.

Tips for Saving Money

Once you’ve found an affordable health insurance plan, there are additional steps you can take to minimize your out-of-pocket expenses:

- Use in-network providers: Health insurance plans have a network of preferred providers who offer discounted rates. Sticking to these providers can significantly reduce your costs.

- Negotiate medical bills: Don’t be afraid to ask for discounts or payment plans from your healthcare providers. Many doctors and hospitals are willing to work with you to make medical care more affordable.

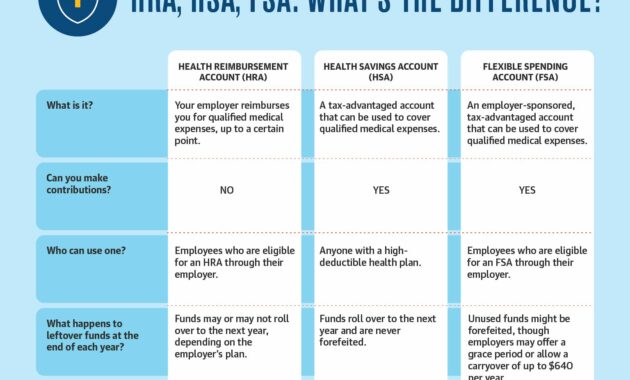

- Use tax-advantaged accounts: Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) allow you to set aside pre-tax dollars to pay for qualified medical expenses, reducing your overall healthcare costs.

Affordable Health Insurance Plans: A Comprehensive Guide to Finding Coverage That Fits Your Budget

In the labyrinthine world of healthcare, securing affordable health insurance plans can feel like a daunting quest. But fear not! With a keen eye for detail and a dash of perseverance, you can navigate this maze and find coverage that won’t break the bank. Let’s embark on a comprehensive journey through the intricacies of health insurance plans, uncovering strategies to keep your premiums within reach.

Understanding Coverage Options

When it comes to health insurance, understanding the different types of coverage is paramount. Each plan varies in terms of benefits, premiums, and deductibles. Here’s a breakdown of the most common coverage options:

- Health Maintenance Organization (HMO): HMOs offer a network of healthcare providers to choose from. You’ll typically have a primary care physician who coordinates your care and refers you to specialists within the network.

- Preferred Provider Organization (PPO): PPOs give you more flexibility in choosing healthcare providers. You can visit any doctor or hospital, but you’ll pay less if you stay within the preferred provider network.

- Point-of-Service (POS) Plan: POS plans are a hybrid of HMOs and PPOs. You have a primary care physician, but you can also see out-of-network providers for an additional cost.

- Fee-for-Service (FFS) Plan: FFS plans allow you to choose any healthcare provider you want. However, you’ll pay the full cost of each visit or procedure.

Utilizing Government Programs

If you’re struggling to afford health insurance, don’t despair. There are several government programs available to assist you:

- ACA Marketplace (Healthcare.gov): The Affordable Care Act (ACA) created marketplaces where individuals and small businesses can shop for and compare health insurance plans. You may also qualify for premium tax credits or cost-sharing reductions to lower your costs.

- Medicaid: Medicaid is a government program that provides health insurance to low-income individuals and families. Coverage varies by state, but Medicaid typically covers a wide range of services, including doctor visits, hospital stays, and prescription drugs.

- Medicare: Medicare is a government program that provides health insurance to people aged 65 and older, as well as certain younger individuals with disabilities.

Taking Advantage of Cost-Saving Measures

Beyond government assistance, there are several ways to reduce the cost of your health insurance premiums:

- Choose a higher deductible: Opting for a higher deductible can lower your monthly premiums. Just make sure you have enough money saved to cover the deductible if you need medical care.

- Increase your out-of-pocket maximum: Setting a higher out-of-pocket maximum can also reduce your premiums. However, you’ll need to pay more for healthcare expenses before your insurance kicks in.

- Use a Health Savings Account (HSA): HSAs allow you to set aside money for healthcare expenses on a pre-tax basis. This can save you money on your income taxes and lower your overall healthcare costs.

- Enroll in a wellness program: Many insurance companies offer wellness programs that can reward you for making healthy choices, such as getting regular checkups or participating in fitness activities.

- Negotiate with your doctor: If you have high medical expenses, you may be able to negotiate a payment plan with your doctor or hospital.

- Consider a lower-cost plan: If you’re healthy and don’t anticipate needing much medical care, a lower-cost plan may be a good option.

- Compare plans: Regularly shop around for health insurance plans to compare costs and coverage. You may be able to find a plan that offers better value for your money.

- Take advantage of discounts: Many insurance companies offer discounts for certain groups, such as employers, students, and seniors.

- Use a broker: A health insurance broker can help you find the right plan for your needs and budget.

Conclusion

Navigating the healthcare system can be a daunting task, but finding affordable health insurance plans doesn’t have to be an insurmountable challenge. By understanding coverage options, utilizing government programs, and taking advantage of cost-saving measures, you can secure coverage that protects your health without breaking the bank. Remember, the path to affordable health insurance is paved with patience, research, and a commitment to finding the solution that works best for you.

{kind=link}