Best Affordable Health Insurance Plans

Health insurance is a must-have in today’s world. It can protect you from financial ruin if you get sick or injured. But with so many different health insurance plans available, it can be tough to know which one is right for you. That’s why we’ve put together this guide to help you find the best affordable health insurance plan for your needs.

Types of Health Insurance Plans

There are four main types of health insurance plans:

- Health Maintenance Organizations (HMOs): HMOs are a type of managed care plan that requires you to choose a primary care physician (PCP). Your PCP will then refer you to specialists if you need to see one. HMOs typically have lower premiums than other types of health insurance plans, but they also have more restrictions on the providers you can see.

- Preferred Provider Organizations (PPOs): PPOs are another type of managed care plan that gives you more flexibility than HMOs. With a PPO, you can choose any doctor or hospital you want, but you’ll pay more for out-of-network care. PPOs typically have higher premiums than HMOs, but they also offer more choice.

- Exclusive Provider Organizations (EPOs): EPOs are a type of managed care plan that is similar to HMOs. However, EPOs do not allow you to see out-of-network providers at all. This can make it difficult to find a doctor if you live in a rural area or if you have a specialized medical condition.

- Point-of-Service (POS) Plans: POS plans are a type of managed care plan that allows you to choose between in-network and out-of-network providers. You’ll pay more for out-of-network care, but you’ll have more flexibility than you would with an HMO or EPO.

How to Find the Best Affordable Health Insurance Plan

Now that you know the different types of health insurance plans available, it’s time to start shopping for a plan. Here are a few tips to help you find the best affordable health insurance plan for your needs:

- Compare plans from multiple insurance companies. Don’t just go with the first plan you find. Take some time to compare plans from different insurance companies to find the one that offers the best coverage at the lowest price.

- Consider your health needs. When choosing a health insurance plan, it’s important to consider your health needs. If you have a chronic condition, you’ll need a plan that covers your condition. You should also consider your age, gender, and family history when choosing a plan.

- Read the plan documents carefully. Before you sign up for a health insurance plan, be sure to read the plan documents carefully. This will help you understand what the plan covers, what the deductibles and co-pays are, and what the exclusions are.

- Talk to a health insurance agent. If you’re not sure which health insurance plan is right for you, you can talk to a health insurance agent. A health insurance agent can help you compare plans and find the one that’s best for your needs.

Best Affordable Health Insurance Plans

Here are a few of the best affordable health insurance plans available:

- Kaiser Permanente: Kaiser Permanente is a non-profit health insurance company that offers a variety of affordable health insurance plans. Kaiser Permanente plans are typically HMOs, which means that you’ll need to choose a primary care physician (PCP). However, Kaiser Permanente also offers PPO plans.

- Blue Cross Blue Shield: Blue Cross Blue Shield is a for-profit health insurance company that offers a variety of affordable health insurance plans. Blue Cross Blue Shield plans are available in all 50 states and the District of Columbia.

- UnitedHealthcare: UnitedHealthcare is a for-profit health insurance company that offers a variety of affordable health insurance plans. UnitedHealthcare plans are available in all 50 states and the District of Columbia.

- Aetna: Aetna is a for-profit health insurance company that offers a variety of affordable health insurance plans. Aetna plans are available in all 50 states and the District of Columbia.

- Cigna: Cigna is a for-profit health insurance company that offers a variety of affordable health insurance plans. Cigna plans are available in all 50 states and the District of Columbia.

Conclusion

Finding the right health insurance plan can be a challenge, but it’s important to do your research and compare plans from different insurance companies. By following the tips in this article, you can find the best affordable health insurance plan for your needs.

Best Affordable Health Insurance Plans: A Comprehensive Guide to Finding the Right Coverage

Navigating the complex world of health insurance can be daunting, especially when affordability is a top priority. Fear not! This comprehensive guide will delve into the intricacies of various health insurance plans, empowering you to make informed decisions that safeguard your well-being without breaking the bank. Join us as we uncover the secrets to finding the best affordable health insurance plans.

Types of Health Insurance Plans

The health insurance landscape offers a spectrum of plans, each tailored to meet specific needs and budgets. Understanding the key distinctions among these plans is crucial for selecting the one that fits you like a glove. Let’s dive into the most prevalent types:

1. Health Maintenance Organizations (HMOs)

HMOs prioritize a network of designated healthcare providers. By restricting access to these providers, HMOs can negotiate lower rates, resulting in more affordable premiums. However, the trade-off lies in the limited choice of doctors and the need for referrals to see specialists. HMOs are particularly suitable for individuals who prefer a consistent healthcare experience within a defined network.

2. Preferred Provider Organizations (PPOs)

PPOs offer a wider range of healthcare providers both within and outside their network. While premiums tend to be higher than HMOs, PPOs provide greater flexibility in selecting doctors and specialists, often without the need for referrals. This freedom comes at a cost, as out-of-network care typically incurs higher expenses. PPOs strike a balance between affordability and choice, making them a popular option for many.

Within the realm of PPOs, we encounter two distinct flavors:

- Exclusive Provider Organizations (EPOs): EPOs closely resemble HMOs in terms of network restrictions. However, they offer slightly more flexibility by allowing members to visit out-of-network providers for a higher cost.

- Point-of-Service (POS) Plans: POS plans bridge the gap between HMOs and PPOs. Members can choose to stay within the network for lower costs or venture outside for a higher price, much like EPOs.

3. Fee-for-Service (FFS) Plans

FFS plans, also known as indemnity plans, provide the ultimate freedom in choosing healthcare providers. However, this flexibility comes with a price tag, as premiums are generally higher than HMOs or PPOs. FFS plans allow members to see any doctor they desire, regardless of network affiliation, and typically require no referrals. This type of plan is often preferred by individuals who value the utmost flexibility and are willing to pay a premium for it.

Factors to Consider When Choosing a Health Insurance Plan

Selecting the best affordable health insurance plan is like assembling a jigsaw puzzle – each piece plays a crucial role in creating the perfect fit. To ensure a seamless experience, consider these key elements:

- Network Size and Provider Availability: HMOs offer smaller networks with limited provider options, while PPOs and FFS plans provide more flexibility. Choose a plan that aligns with your preferred healthcare providers and locations.

- Premium Costs: Premiums are the recurring payments you make for your health insurance coverage. HMOs typically have lower premiums than PPOs and FFS plans due to their restricted networks.

- Deductibles and Copayments: Deductibles represent the amount you pay out-of-pocket before your insurance coverage kicks in. Copayments are fixed amounts you pay for specific healthcare services. Higher deductibles and copayments often result in lower premiums.

- Out-of-Pocket Maximums: This is the maximum amount you’ll have to pay for covered healthcare expenses in a year. Once you reach this limit, your insurance will cover 100% of eligible costs.

- Coverage for Specific Services: Carefully scrutinize the plan’s coverage details to ensure it aligns with your healthcare needs. Pay attention to mental health coverage, prescription drug benefits, and other essential services.

Tips for Finding Affordable Health Insurance Plans

Affordability is paramount when selecting a health insurance plan. Here are some savvy tips to help you save:

- Shop Around: Don’t settle for the first plan you come across. Compare quotes from multiple insurance providers to find the best deal.

- Consider a High-Deductible Health Plan (HDHP): HDHPs offer lower premiums but higher deductibles. If you’re generally healthy and don’t anticipate significant healthcare expenses, an HDHP can be a cost-effective option.

- Take Advantage of Employer-Sponsored Plans: If your employer offers health insurance, it’s often the most affordable way to secure coverage.

- Explore Government Subsidies: Low- and moderate-income individuals may qualify for government subsidies to help cover the cost of health insurance premiums.

- Negotiate with Your Provider: Don’t be afraid to negotiate with your health insurance provider. In some cases, you may be able to secure a lower premium or more favorable terms.

Finding the best affordable health insurance plan is not just about saving money; it’s about safeguarding your health and well-being. By understanding the different types of plans and carefully considering your needs and budget, you can make an informed decision that provides peace of mind and financial protection.

Best Affordable Health Insurance Plans: A Comprehensive Guide to Finding the Perfect Fit

Navigating the complex healthcare landscape can be daunting. Choosing the right health insurance plan is crucial for protecting your health and well-being without breaking the bank. That’s why we’ve compiled this comprehensive guide to help you find the best affordable health insurance plans that meet your unique needs.

1. Determine Your Needs

The first step is to assess your health insurance needs. Consider your age, overall health, and lifestyle. If you’re young and healthy, you may opt for a basic plan with lower premiums. However, if you have chronic conditions or expect significant medical expenses, a more comprehensive plan would be advisable.

2. Compare Plan Types

There are several types of health insurance plans available, including HMOs, PPOs, and POSs. Each type offers different benefits and restrictions. HMOs typically have lower premiums but limit you to a network of providers. PPOs provide more flexibility but come with higher premiums. POSs strike a balance between HMOs and PPOs.

3. Explore Affordable Health Insurance Options

Now let’s dive into the nitty-gritty of finding affordable health insurance plans. Here are some tips to help you navigate the complexities:

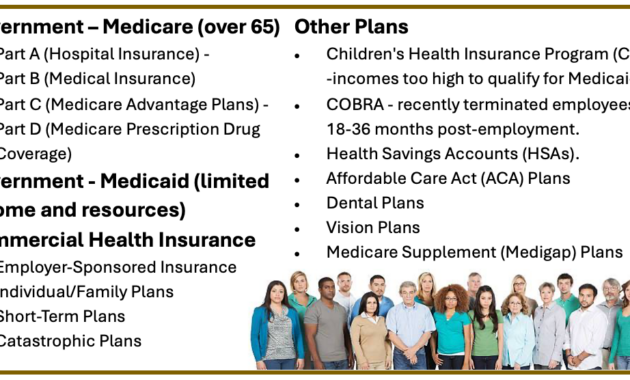

a. **Government Assistance:** Low-income individuals and families may qualify for government-sponsored programs like Medicaid and CHIP, which provide comprehensive health coverage at minimal cost or no cost at all.

b. **Employer-Sponsored Plans:** Most employers offer group health insurance plans that can be more affordable than individual policies. Check with your employer to see if you’re eligible.

c. **Catastrophic Health Plans:** These plans are designed for younger, healthy individuals who may not require extensive medical care. They offer low premiums but have high deductibles and fewer benefits.

d. **Short-Term Health Insurance:** These temporary plans can provide coverage for a limited period, such as between jobs or during a gap in coverage. They are typically more affordable than traditional health insurance plans.

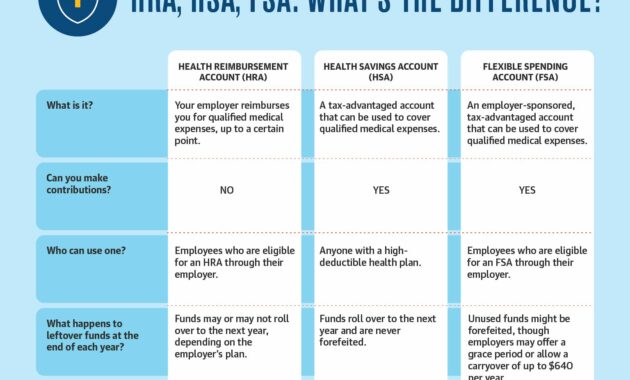

e. **Health Savings Accounts (HSAs):** HSAs are paired with high-deductible health plans and allow you to save money tax-free for qualified medical expenses. This can help reduce your overall healthcare costs.

f. **Health Maintenance Organizations (HMOs):** HMOs typically offer lower premiums than other plan types, but they may restrict your choice of providers to a specific network. In some cases, HMOs may also require you to get a referral from a primary care physician before seeing a specialist.

g. **Preferred Provider Organizations (PPOs):** PPOs generally offer more flexibility than HMOs, allowing you to see providers outside of the network, though you may pay higher costs. PPOs typically have higher premiums than HMOs, but they may offer more comprehensive coverage.

h. **Point-of-Service (POS) Plans:** POS plans combine features of both HMOs and PPOs. They offer more flexibility than HMOs, but they may also have higher premiums. POS plans typically require you to choose a primary care physician, but you may be able to see specialists outside of the network with a referral.

i. **Indemnity Plans:** Indemnity plans are a type of health insurance that provides you with a fixed amount of money to cover your medical expenses. You can use this money to see any provider you want, but you may have to pay more out-of-pocket costs than you would with other types of health insurance plans.

4. Get Quotes and Compare

Once you have a better understanding of your needs and the available options, it’s time to get quotes from different insurance companies. Be sure to compare plans carefully, considering factors like premiums, deductibles, co-pays, and out-of-pocket maximums.

5. Make an Informed Decision

Choosing the right health insurance plan is a crucial decision that requires careful consideration. Weigh the pros and cons of each option and select the plan that best meets your needs and budget. Remember, it’s not just about finding the most affordable plan but also about finding the plan that provides the coverage you need.

With this comprehensive guide as your compass, you can navigate the complexities of health insurance and secure the best affordable plan for your peace of mind and well-being.

{kind=link}