Affordable Health Insurance Plans for Young Adults

Finding the Right Fit

Navigating the labyrinth of health insurance options can be a daunting task, especially for young adults. With a plethora of plans available, each promising a laundry list of benefits, finding the one that suits your specific needs and budget can feel like an impossible riddle. But fret not, young adventurers, for this comprehensive guide will illuminate the path to securing affordable health insurance. Let’s dive in!

Unveiling the Secrets of Deductibles

Deductibles, the initial amount you pay out of pocket before your insurance kicks in, can have a significant impact on your monthly premiums. The higher the deductible, the lower your premiums. But remember, a higher deductible means more financial responsibility in the event of unexpected medical expenses. It’s like a balancing act, where you weigh the potential savings against the risk of having to shell out more cash upfront.

Copays and Coinsurance: Unmasking the Hidden Costs

Copays, those fixed amounts you pay for certain medical services like doctor’s visits or prescriptions, can add up over time. Coinsurance, on the other hand, is a percentage of the total cost of medical care that you’re responsible for. These seemingly insignificant costs can accumulate, so be sure to factor them into your budget when selecting a plan.

In-Network vs. Out-of-Network: Navigating the Provider Maze

In-network providers are those who have contracted with your insurance company to offer discounted rates for their services. Staying within your network can save you significant money, but it may limit your choice of doctors and hospitals. Out-of-network providers, while more expensive, offer greater flexibility in choosing your healthcare providers.

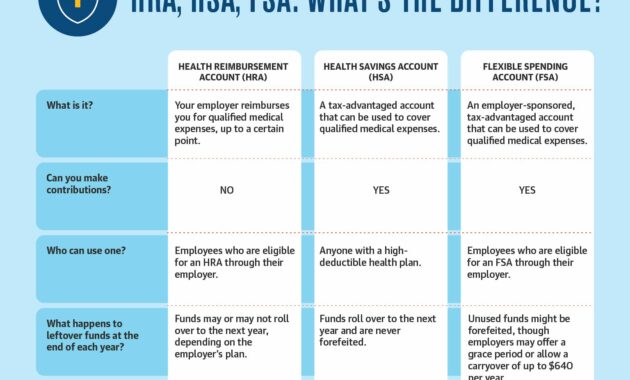

HSA and FSA: Tax-Saving Strategies

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) can help you save money on healthcare expenses. HSAs are tax-advantaged accounts that allow you to save money for qualified medical expenses. FSAs are employer-sponsored accounts that allow you to set aside pre-tax dollars for healthcare expenses. These accounts can help reduce your overall healthcare costs.

Affordable Health Insurance Options for Young Adults

-

Catastrophic Health Plans: Designed for young adults who are generally healthy and don’t anticipate major medical expenses, these plans offer low monthly premiums but high deductibles.

-

Bronze Plans: These plans have higher deductibles and lower monthly premiums compared to other plans. They offer basic coverage for essential health services.

-

Silver Plans: Silver plans offer a balance between deductibles and monthly premiums. They cover a wider range of health services compared to bronze plans.

-

Gold Plans: Gold plans have lower deductibles and higher monthly premiums. They offer comprehensive coverage for a wide range of health services.

-

Platinum Plans: Platinum plans offer the most comprehensive coverage with the lowest deductibles. However, they come with the highest monthly premiums.

Tailoring the Plan to Your Lifestyle

When selecting a health insurance plan, consider your age, health status, and lifestyle. If you’re young and healthy, a catastrophic or bronze plan may be a good fit. If you have a chronic condition or anticipate significant medical expenses, a silver, gold, or platinum plan may be more appropriate. It’s like customizing a suit—find the plan that fits your unique needs and budget like a glove.

The Benefits of Health Insurance

-

Peace of Mind: Health insurance provides a safety net, giving you peace of mind knowing that you’re protected against unexpected medical expenses.

-

Access to Care: With health insurance, you have access to a wide range of healthcare services, including preventive care, doctor’s visits, and hospital stays.

-

Financial Protection: Health insurance can help you avoid the financial burden of major medical expenses, which can be crippling without coverage.

-

Long-Term Health: Health insurance promotes long-term health by encouraging preventive care and early detection of health issues.

Conclusion

Finding affordable health insurance as a young adult doesn’t have to be an insurmountable task. By understanding the different types of plans, deductibles, copays, and coinsurance, you can make an informed decision that meets your needs and budget. Remember, health insurance is an investment in your future health and financial well-being. Don’t be afraid to ask questions, compare plans, and seek professional advice to find the perfect fit for you.

Affordable Health Insurance Plans for Young Adults: A Comprehensive Guide

As a young adult, navigating the complexities of health insurance can feel like a daunting task. With so many plans and options available, finding the right coverage that fits your needs and budget can be a challenge. This guide will provide you with all the essential information you need to understand your options and make an informed decision about your health insurance coverage.

Understanding Your Options

Navigating the world of health insurance plans can feel like stepping into a maze filled with unfamiliar terms and confusing choices. To make sense of it all, let’s unravel the three main types of health insurance plans that young adults can consider: Marketplace plans, employer-sponsored plans, and Medicaid or CHIP.

Marketplace Plans: A Gateway to AffordableCoverage

Marketplace plans, also known as Affordable Care Act (ACA) plans, are a government-regulated option that provides health insurance to individuals and families who do not have access to employer-sponsored coverage. These plans are available through HealthCare.gov or your state’s insurance marketplace, and they offer a range of coverage options and subsidies to make health insurance more affordable for low- and moderate-income individuals and families.

Enrollment Periods: Open enrollment for Marketplace plans runs from November 1st to January 15th each year. During this time, you can shop for plans, compare coverage, and enroll in the plan that best suits your needs. If you miss the open enrollment period, you may still be able to enroll in a Marketplace plan if you qualify for a special enrollment period due to a qualifying life event, such as a job loss or a change in income.

Types of Marketplace Plans: Marketplace plans come in four different coverage levels, each offering varying levels of coverage and cost. Bronze plans have the lowest monthly premiums but provide the least coverage. Silver plans offer more comprehensive coverage than Bronze plans, but they come with higher premiums. Gold plans provide even more comprehensive coverage than Silver plans, but they also have higher premiums. Platinum plans offer the most comprehensive coverage, but they also have the highest premiums.

Subsidies and Tax Credits: To make Marketplace plans more affordable, the government offers subsidies and tax credits to low- and moderate-income individuals and families. These subsidies are based on your income and family size, and they can significantly reduce the cost of your monthly premiums.

Employer-Sponsored Plans: Coverage Through Your Job

Employer-sponsored health insurance plans are provided by your employer as a benefit of your employment. These plans are often more affordable than Marketplace plans, and they may offer a wider range of coverage options. However, you may not be eligible for an employer-sponsored plan if you do not work for a company that offers health insurance coverage.

Types of Employer-Sponsored Plans: Employer-sponsored health insurance plans can come in two different types: Preferred Provider Organizations (PPOs) and Health Maintenance Organizations (HMOs). PPOs offer more flexibility than HMOs, but they may also have higher premiums. HMOs offer lower premiums than PPOs, but they may have more restrictions on which doctors and hospitals you can see.

Contribution Options: With employer-sponsored plans, your employer may contribute a portion of the premium cost, making your coverage even more affordable. The amount of your employer’s contribution will vary depending on the plan and your employer’s policies.

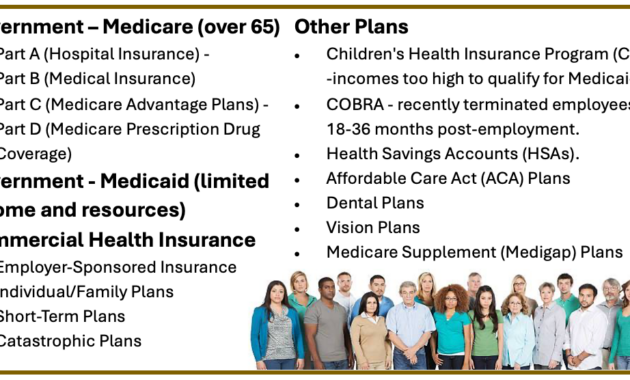

Medicaid or CHIP: Coverage for Low-Income Individuals and Families

Medicaid and CHIP (Children’s Health Insurance Program) are government-funded health insurance programs that provide coverage to low-income individuals and families. These programs are available to people of all ages, but they have specific eligibility requirements based on income and family size.

Medicaid: Medicaid is a joint federal and state program that provides health insurance to low-income individuals and families. Eligibility for Medicaid varies from state to state, but it is generally available to pregnant women, children, and disabled individuals.

CHIP: CHIP is a federal program that provides health insurance to children and young adults from low-income families. Eligibility for CHIP varies from state to state, but it is generally available to children and young adults under the age of 19 who are not eligible for Medicaid.

Now that you have a better understanding of the different types of health insurance plans available to young adults, let’s explore some of the factors you should consider when choosing a plan that’s right for you.

Affordable Health Insurance Plans for Young Adults: Your Guide to Saving Money While Staying Healthy

If you’re a young adult, you know that health insurance can be a major expense. But don’t worry – there are ways to find affordable plans that fit your needs and budget.

One of the best places to start is the Health Insurance Marketplace. This government-run website makes it easy to compare plans and find the right one for you.

Navigating the Marketplace

The Marketplace is a great way to find affordable health insurance plans, but it can be a bit overwhelming at first. Here are a few tips to help you get started:

- Create an account. The first step is to create an account on the Marketplace website. This will allow you to save your information and compare plans.

- Enter your information. Once you’ve created an account, you’ll need to enter some basic information about yourself, such as your age, income, and ZIP code. This information will help the Marketplace find plans that are right for you.

- Compare plans. Once you’ve entered your information, you’ll be able to compare plans from different insurance companies. Be sure to compare the monthly premiums, deductibles, copayments, and other costs.

- Choose a plan. Once you’ve found a plan that you like, you can enroll online or over the phone. You’ll need to provide some additional information, such as your Social Security number and bank account information.

Understanding Health Insurance Plans

Once you’ve enrolled in a health insurance plan, it’s important to understand how it works. Here are a few key terms to know:

- Premium: The premium is the monthly payment you make for your health insurance plan.

- Deductible: The deductible is the amount of money you have to pay out-of-pocket before your insurance starts to cover costs.

- Copayment: A copayment is a fixed amount of money that you pay for certain medical services, such as doctor’s visits or prescriptions.

- Coinsurance: Coinsurance is a percentage of the cost of a medical service that you pay after you’ve met your deductible.

Finding Affordable Plans for Young Adults

There are a few things you can do to find affordable health insurance plans for young adults:

- Shop around. Compare plans from different insurance companies before you make a decision. You may be able to find a plan that’s cheaper than the one you’re currently enrolled in.

- Consider a high-deductible plan. High-deductible plans have lower monthly premiums, but they also have higher deductibles. If you’re healthy and don’t expect to have many medical expenses, a high-deductible plan could be a good option for you.

- Get a subsidy. If you have a low income, you may be eligible for a subsidy that can help you pay for your health insurance premiums.

Affordable Health Insurance Plans for Young Adults

Navigating the healthcare landscape as a young adult can be a daunting task, especially when it comes to finding affordable health insurance plans. The good news is that there are options available to help you get the coverage you need without breaking the bank. Let’s dive into the ins and outs of health insurance for young adults, exploring everything from employer-sponsored plans to government subsidies and individual insurance marketplaces.

Employer-Sponsored Plans

If you’re fortunate enough to have an employer who offers health insurance, this may be your most cost-effective option. Employer-sponsored plans often come with lower premiums and deductibles than individual plans, and your employer may even contribute a portion of the premiums.

Weighing the Pros and Cons

Pros:

- Lower premiums and deductibles

- Employer contributions to premiums

- Access to a wider range of plans and benefits

- Convenient enrollment and administration

Cons:

- Limited plan options if your employer only offers a few plans

- Coverage may be tied to your employment status

- May not be available in all jobs or industries

Understanding Premiums, Deductibles, and Copays

When evaluating employer-sponsored plans, it’s crucial to understand the key terms:

- Premium: The monthly payment you make for your health insurance coverage.

- Deductible: The amount you must pay out of pocket for medical expenses before your insurance starts covering costs.

- Copay: A fixed amount you pay for specific medical services, such as doctor’s visits or prescription drugs.

By carefully considering these factors, you can make an informed decision about whether an employer-sponsored plan is the right choice for you.

Affordable Health Insurance Plans for Young Adults

Navigating the world of health insurance can be a daunting task, especially for young adults. With the rising costs of healthcare, finding affordable coverage can feel like an insurmountable challenge. However, there are options available to help make health insurance more accessible for this age group. This article will delve into the various affordable health insurance plans tailored to young adults, exploring their benefits, eligibility criteria, and where to find them. We’ll also address common misconceptions and provide tips for choosing the right plan that meets your individual needs.

Medicaid and CHIP

For low-income young adults, Medicaid and the Children’s Health Insurance Program (CHIP) offer potential coverage options. Medicaid is a government-funded health insurance program that provides comprehensive coverage for individuals and families with limited financial resources. CHIP is similar to Medicaid, but it specifically targets children and young adults up to age 19. Both programs have income eligibility requirements that vary by state, so it’s important to check with your local Medicaid or CHIP agency to determine if you qualify.

Understanding Medicaid and CHIP Eligibility

Eligibility for Medicaid and CHIP depends on several factors, including income, family size, and state of residence. In general, individuals and families with incomes below a certain threshold qualify for coverage. The specific income limits vary from state to state, so it’s essential to contact your local agency for more information. Additionally, some states have expanded Medicaid eligibility under the Affordable Care Act (ACA), which may provide coverage to more low-income young adults.

Benefits of Medicaid and CHIP

Medicaid and CHIP offer a wide range of benefits for enrollees, including coverage for doctor visits, hospital stays, prescription drugs, and mental health services. These programs play a crucial role in ensuring that low-income young adults have access to essential healthcare services, regardless of their ability to pay. By providing comprehensive coverage, Medicaid and CHIP help improve health outcomes and reduce financial burdens.

Applying for Medicaid and CHIP

Applying for Medicaid or CHIP is typically a straightforward process. Individuals can apply online, by mail, or in person at their local Medicaid or CHIP office. The application process involves providing information about your income, family size, and other relevant details. Once your application is submitted, it will be reviewed to determine your eligibility. If you qualify, you will be enrolled in the program and issued a health insurance card.

Additional Resources for Medicaid and CHIP

Numerous resources are available to help young adults learn more about Medicaid and CHIP and apply for coverage. The following websites provide detailed information and assistance:

Medicaid.gov: https://www.medicaid.gov/

CHIP.gov: https://www.chip.gov/

The National Association of Medicaid Directors (NAMD): https://www.medicaiddirectors.org/

Affordable Health Insurance Plans for Young Adults: A Comprehensive Guide

Navigating the world of health insurance as a young adult can seem like a daunting task. The good news? There are a plethora of affordable options available, tailored specifically to meet your needs and budget. In this article, we’ll delve into all things health insurance, from understanding the basics to finding the plan that fits you like a glove, empowering you to make informed decisions about your health coverage.

Who Qualifies as a Young Adult?

In the realm of health insurance, young adulthood typically spans from the tender age of 18 to the ripe old age of 26. During this time, you may have the privilege of remaining on your parents’ health insurance plan. However, once you spread your wings and venture out on your own, securing your own health coverage becomes essential.

Types of Health Insurance Plans

There’s no shortage of health insurance plans to choose from, each with its own unique set of benefits and drawbacks. Let’s break down the most common types:

- Health Maintenance Organizations (HMOs): HMOs keep things cozy by limiting your healthcare providers to a specific network. In return for this exclusivity, you’ll enjoy lower premiums and out-of-pocket costs.

- Preferred Provider Organizations (PPOs): PPOs offer more flexibility than HMOs, allowing you to venture outside their network, albeit at a higher cost.

- Exclusive Provider Organizations (EPOs): EPOs resemble HMOs in their network limitations, but they tend to have lower premiums and deductibles.

- Point-of-Service (POS) Plans: POS plans combine the best of both worlds—the lower costs of HMOs and the flexibility of PPOs.

- High-Deductible Health Plans (HDHPs): HDHPs come with lower premiums, but they require you to pay a higher deductible before the insurance starts kicking in.

Finding Affordable Health Insurance Plans

Ready to embark on your search for affordable health insurance? Here’s a game plan to guide you:

- Assess Your Needs: Take stock of your health status, medications, and expected medical expenses. This will help you determine the level of coverage you need.

- Compare Plans: Don’t settle for the first plan that crosses your path. Shop around, compare premiums, deductibles, and coverage. Online marketplaces like Healthcare.gov can streamline this process.

- Consider Your Budget: Health insurance can put a dent in your wallet, so set a budget before you start exploring options. Factor in both monthly premiums and potential out-of-pocket expenses.

- Take Advantage of Subsidies: If you qualify, subsidies can make health insurance more affordable. Check your eligibility on Healthcare.gov.

Additional Tips

Beyond finding the right plan, here are a few money-saving tips to keep in your back pocket:

- Use Preventive Care Services: Regular checkups and screenings can help you catch health issues early on, potentially saving you big bucks in the long run.

- Participate in Wellness Programs: Many health insurers offer wellness programs that reward you for healthy habits, such as quitting smoking or losing weight.

- Negotiate with Providers: Don’t be afraid to ask for discounts or payment plans if you’re struggling to afford medical expenses.

- Take Advantage of Generic Drugs: Generic medications are just as effective as brand-name drugs, but they cost significantly less.

- Use a Health Savings Account (HSA): HSAs are tax-advantaged accounts that allow you to save money for medical expenses on a pre-tax basis.

- Consider Tax Credits: If you’re self-employed or have low income, you may qualify for tax credits that can reduce your health insurance costs.

Conclusion

Securing affordable health insurance as a young adult is not an impossible feat. By understanding the types of plans available, comparing options, and taking advantage of money-saving tips, you can find a plan that fits your needs and budget. Remember, health insurance is an investment in your well-being, and it’s never too early to start protecting your health.

So, what are you waiting for? Dive into the world of health insurance and empower yourself with the coverage you deserve. Your future self will thank you for it!

{kind=link}