Health Insurance Affordable Plans

Health insurance is a safety net that protects you from unexpected medical expenses. With so many plans available, finding one that fits your budget and needs can be overwhelming. This article will guide you through the process of choosing an affordable health insurance plan, covering everything from plan types to additional considerations.

Types of Health Insurance Plans

There are four main types of health insurance plans:

- Health Maintenance Organizations (HMOs): HMOs offer a network of providers and facilities that you must use for your care. They typically have lower premiums than other plans but may have more restrictions on your choice of providers.

- Preferred Provider Organizations (PPOs): PPOs offer a wider network of providers than HMOs, and you can choose to go outside the network if you’re willing to pay a higher cost. PPOs typically have higher premiums than HMOs but offer more flexibility.

- Exclusive Provider Organizations (EPOs): EPOs are similar to HMOs, but they have a narrower network of providers. They typically have lower premiums than HMOs but may have more restrictions on your choice of providers.

- Point-of-Service (POS) Plans: POS plans combine features of HMOs and PPOs. You typically have a primary care physician who coordinates your care, but you can also see specialists outside the network if you’re willing to pay a higher cost. POS plans typically have premiums that are in between HMOs and PPOs.

Choosing an Affordable Plan

When choosing an affordable health insurance plan, there are several factors to consider:

- Monthly Premium: The monthly premium is the amount you pay each month for your health insurance. Premiums vary depending on the type of plan, your age, and your location.

- Deductible: The deductible is the amount you must pay out-of-pocket before your insurance starts to cover your medical expenses. Higher deductibles typically result in lower premiums.

- Coinsurance: Coinsurance is the percentage of your medical expenses that you must pay after you’ve met your deductible. Higher coinsurance typically results in lower premiums.

- Copay: A copay is a fixed amount that you pay for certain medical services, such as doctor’s visits or prescription drugs. Copays are typically lower than coinsurance.

Additional Considerations

In addition to the factors listed above, there are several other considerations to keep in mind when choosing an affordable health insurance plan:

Network of Providers

The network of providers is the group of doctors and hospitals that your health insurance plan covers. It’s important to make sure that your plan includes the providers you want to see. You can typically find a list of providers on your insurance company’s website.

Premium Costs

The premium cost is the amount you pay each month for your health insurance. Premiums vary depending on the type of plan, your age, and your location. You can typically get a quote for a health insurance plan by calling your insurance company or visiting their website.

Coverage Limitations

Coverage limitations are the restrictions on what your health insurance plan covers. For example, some plans may not cover certain types of medical treatments or may have limits on the amount of coverage you can receive. It’s important to read the plan details carefully before you enroll to make sure that you understand the coverage limitations.

Other Considerations

In addition to the factors discussed above, there are several other considerations to keep in mind when choosing an affordable health insurance plan:

- Your health status: If you have a chronic illness or condition, you’ll want to make sure that your health insurance plan covers the treatments you need.

- Your family size: If you have a family, you’ll need to make sure that your health insurance plan covers all of your family members.

- Your budget: It’s important to make sure that you can afford the monthly premium for your health insurance plan.

- Your risk tolerance: If you’re willing to take on more risk, you can choose a plan with a higher deductible or coinsurance in exchange for a lower premium.

- Your future plans: If you’re planning to have a family or change jobs in the future, you’ll want to make sure that your health insurance plan will meet your needs.

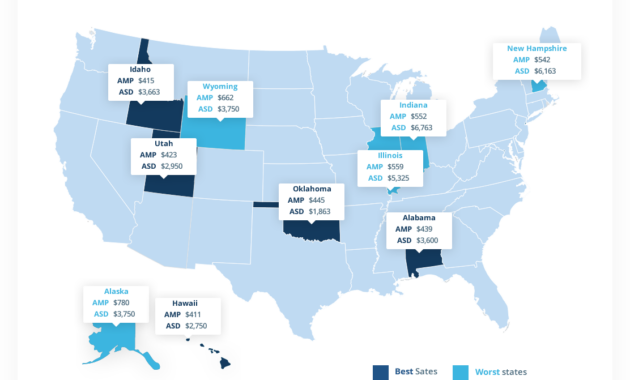

- Your state’s regulations: Health insurance regulations vary from state to state. It’s important to make sure that you understand the regulations in your state before you enroll in a health insurance plan.

- Your employer’s coverage: If you have an employer, they may offer health insurance coverage. It’s important to compare your employer’s plan to other plans before you enroll.

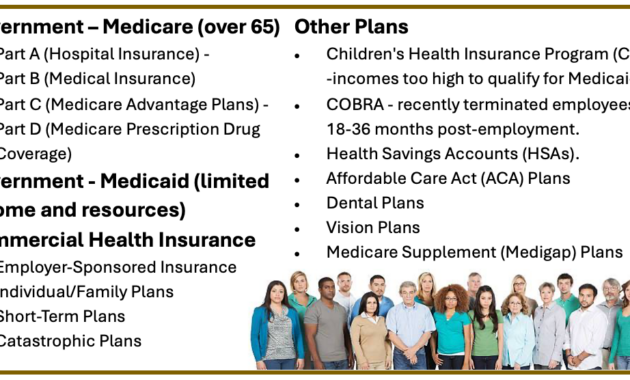

- Government assistance programs: If you have low income, you may be eligible for government assistance programs that can help you pay for health insurance. These programs include Medicaid and CHIP.

Conclusion

Choosing an affordable health insurance plan can be a daunting task, but it’s important to remember that you’re not alone. There are many resources available to help you make the best decision for your needs. By taking the time to compare plans and consider your individual circumstances, you can find a health insurance plan that fits your budget and protects you from unexpected medical expenses.

{kind=link}