Affordable Family Health Insurance Plans

In the United States, health insurance is a complex and often confusing landscape. With so many different plans and providers to choose from, it can be difficult to know where to start. And when you’re trying to find affordable health insurance for your family, the task can seem even more daunting.

But don’t despair! There are affordable family health insurance plans available. You just need to know where to look. Here are a few tips to help you get started:

1. **Start by exploring your employer-sponsored plan.** If you’re employed, your employer may offer health insurance as a benefit. This is often the most affordable option, so it’s worth checking into. Even if you don’t think your employer offers health insurance, it’s still worth asking. Some employers offer health insurance as a voluntary benefit, so you may be able to add it to your benefits package even if it’s not offered as a standard benefit.

2. **If you’re not eligible for employer-sponsored insurance, you can purchase a plan through the Health Insurance Marketplace.** The Health Insurance Marketplace is a government-run website where you can compare plans and prices from different insurers. You may also be eligible for subsidies to help you pay for your premiums. The open enrollment period for the Health Insurance Marketplace runs from November 1st to January 15th.

3. **Consider a Health Savings Account (HSA).** An HSA is a tax-advantaged savings account that you can use to pay for qualified medical expenses. HSAs are available to individuals and families who are enrolled in a high-deductible health plan (HDHP). HDHPs have lower premiums than traditional health insurance plans, but they also have higher deductibles. If you’re healthy and don’t expect to have many medical expenses, an HSA can be a good way to save money on health insurance.

Here is an affordable family health insurance plan many have found helpful:

**The bronze plan** is the most affordable type of health insurance plan. It has a lower monthly premium, but it also has a higher deductible and coinsurance. This means that you will have to pay more out of pocket for medical expenses before your insurance starts to cover them.

Here are some additional tips for finding affordable family health insurance:

• **Shop around.** Don’t just go with the first plan you find. Compare plans from different insurers to find the one that’s right for you and your family.

• Consider your family’s health needs. If you have a family member with a chronic condition, you’ll need to make sure that the plan you choose covers their needs.

• Read the fine print. Make sure you understand what the plan covers and what it doesn’t cover. You don’t want to be surprised by hidden costs later on.

• Ask for help. If you’re having trouble finding affordable family health insurance, you can get help from a health insurance agent or broker. They can help you compare plans and find the one that’s right for you.

Finding affordable family health insurance can be a challenge, but it’s not impossible. By following these tips, you can find a plan that meets your needs and your budget.

**Additional Resources:**

• [Health Insurance Marketplace](https://www.healthcare.gov/)

• Health Savings Accounts (HSAs)

• National Association of Insurance Commissioners (NAIC)

Affordable Family Health Insurance: Navigating the Maze for Optimum Coverage

In today’s healthcare landscape, safeguarding your family’s well-being is paramount. Affordable family health insurance plans can serve as the bedrock of financial protection, shielding your loved ones from unexpectedly high medical expenses. However, navigating the myriad options available can be a daunting task. Here’s a comprehensive guide to help you make an informed decision and secure the coverage that fits your needs and budget.

Types of Family Health Insurance Plans

There’s a wide array of family health insurance plans on the market, each with its unique advantages and drawbacks. Understanding the different types can empower you to make the best choice for your family.

Managed Care Plans: A Cost-Effective Approach

Managed care plans, such as Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs), offer cost-effective coverage by channeling medical care through a network of designated providers. HMOs typically have lower premiums but may restrict your access to healthcare services, while PPOs provide more flexibility and a wider choice of providers, albeit with higher premiums.

Fee-for-Service Plans: Flexibility and Autonomy

Fee-for-service plans, also known as indemnity plans, grant you the freedom to choose any healthcare provider without network restrictions. However, this flexibility comes at a premium, as these plans tend to have higher out-of-pocket expenses and annual deductibles.

Consumer-Driven Health Plans: Empowering You with Control

Consumer-driven health plans (CDHPs), such as Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs), offer a tax-advantaged way to pay for healthcare expenses. CDHPs typically involve higher deductibles but allow you to save money in the long run by contributing pre-tax dollars to an account that can be used for eligible medical expenses.

Choosing the Right Plan: Balancing Cost and Coverage

Selecting the optimal family health insurance plan hinges on striking a delicate balance between cost and coverage. Consider your family’s health needs, budget, and risk tolerance when assessing the following factors:

Premiums: Premiums are the monthly payments you make for insurance coverage. Lower premiums can be tempting, but remember, they often come with higher deductibles and out-of-pocket expenses.

Deductibles: Deductibles are the amount you must pay out of pocket before insurance coverage kicks in. Higher deductibles can reduce premiums, but they require you to shoulder more medical expenses yourself.

Out-of-Pocket Maximums: Out-of-pocket maximums cap your financial liability for healthcare expenses within a plan year. Lower out-of-pocket maximums provide greater financial protection, but they may come with higher premiums.

Provider Networks: Managed care plans limit your access to healthcare providers within their networks. Consider whether the network includes your preferred providers or if you value the flexibility of choosing any provider.

Coverage Inclusions and Exclusions: Carefully review the plan’s coverage inclusions and exclusions to ensure it meets your family’s specific healthcare needs. Some plans may not cover certain treatments or services, so it’s essential to verify that your family’s medical requirements are adequately covered.

Choosing an Affordable Family Health Insurance Plan

Finding affordable family health insurance can be challenging, but it’s not impossible. Consider the following strategies to reduce your premiums:

Shop Around and Compare Plans: Compare quotes from multiple insurance providers to find the most competitive rates. Don’t be afraid to negotiate with insurance agents to secure the best possible deal.

Explore Employer-Sponsored Plans: If you’re employed, inquire about your employer’s health insurance options. Employer-sponsored plans often offer lower premiums and better benefits than individual plans.

Consider a High-Deductible Health Plan (HDHP): HDHPs typically have lower premiums but come with higher deductibles. If you’re healthy and don’t anticipate frequent medical expenses, an HDHP can be an affordable option.

Maximize Tax Credits and Subsidies: Low- and middle-income families may qualify for tax credits or subsidies that can significantly reduce the cost of health insurance. Explore these options through your state’s health insurance exchange or the federal marketplace.

Conclusion

Securing affordable family health insurance is essential for safeguarding your family’s well-being in today’s healthcare environment. By understanding the different types of plans, carefully considering your needs and budget, and exploring available strategies to reduce costs, you can make an informed decision that provides the optimal coverage for your family. Remember, a comprehensive health insurance plan is an investment in your family’s future, ensuring peace of mind and financial protection when you need it most.

Affordable Family Health Insurance Plan: A Comprehensive Guide

Navigating the world of health insurance can be a daunting task, especially when it comes to finding an affordable plan for your family. The stakes are high, and you don’t want to compromise on quality or run the risk of being financially overwhelmed. That’s why we’re here to guide you through the process, breaking down the essential considerations and providing you with tips to find the best possible plan that meets your family’s unique needs.

Choosing the Right Plan

When it comes to selecting a family health insurance plan, there’s no one-size-fits-all solution. Every family’s circumstances are different, so it’s crucial to weigh a few key factors:

1. Family Size and Age Ranges:

The number of people in your family and their age ranges will significantly impact the cost of your plan. Generally, plans with more dependents are more expensive, and children and older adults tend to have higher healthcare expenses.

2. Budget:

Health insurance premiums can vary widely, so it’s essential to determine how much you can afford to allocate towards monthly payments. Don’t forget to factor in potential out-of-pocket expenses like deductibles and copayments.

3. Health Needs:

Your family’s current and anticipated health needs should play a significant role in your plan selection. Consider any pre-existing conditions, chronic illnesses, or anticipated surgeries. Plans with higher coverage levels tend to come with higher premiums, but they may provide greater peace of mind in the long run.

4. Types of Coverage:

There are different types of health insurance plans available, each with its own set of benefits and limitations.

– HMO (Health Maintenance Organization): HMOs offer comprehensive coverage through a network of healthcare providers, but they may have limitations on who you can see and where you can receive care.

– PPO (Preferred Provider Organization): PPOs provide more flexibility in choosing your healthcare providers, but out-of-network care may be more expensive.

– EPO (Exclusive Provider Organization): EPOs are similar to HMOs but offer a narrower network of providers.

– POS (Point-of-Service Plan): POS plans combine features of both HMOs and PPOs, allowing you to choose providers within a network or pay extra to go out-of-network.

Finding an Affordable Plan

Now that you have a better understanding of your family’s needs, let’s explore some tips for finding an affordable plan:

1. Compare Quotes from Multiple Providers:

Don’t limit yourself to one insurance company. Get quotes from several providers to compare premiums, coverage levels, and plan options.

2. Consider High-Deductible Plans:

High-deductible plans have lower monthly premiums, but they also require you to pay more out-of-pocket costs before your insurance kicks in. If your family is generally healthy and has infrequent healthcare expenses, this option could save you money.

3. Take Advantage of Tax Credits:

The government offers tax credits to help low- and moderate-income families afford health insurance. Be sure to check your eligibility and take advantage of these credits if you qualify.

4. Look for Employer-Sponsored Plans:

If you or your spouse have access to an employer-sponsored plan, be sure to explore its features and cost. Employer-sponsored plans may offer more affordable options than individual plans.

Conclusion

Finding an affordable family health insurance plan is possible with some research and planning. By following these tips, you can find a plan that meets your family’s unique needs and provides peace of mind without breaking the bank.

Affordable Family Health Insurance Plans: Essential Coverage for a Healthy Family

Navigating the healthcare landscape as a family can be a daunting task, especially when it comes to finding an affordable health insurance plan. But with careful consideration and research, you can secure comprehensive coverage that safeguards your family’s well-being without breaking the bank.

This article delves into the nuances of affordable family health insurance plans, providing valuable insights and practical tips to help you make informed decisions. We’ll explore key considerations, plan options, and strategies to maximize the benefits of your coverage.

Exploring Affordable Family Health Insurance Options

The first step towards finding an affordable family health insurance plan is understanding your options. Employer-sponsored plans are often a good starting point, but if you’re self-employed or not eligible for coverage through work, you can explore the following options:

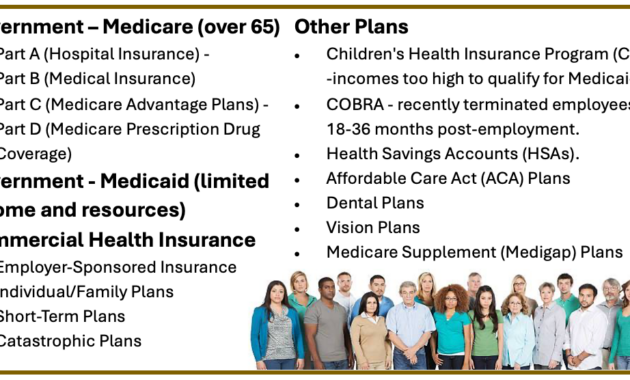

- Health Insurance Marketplace: The Health Insurance Marketplace, also known as Obamacare, offers a range of plans and subsidies based on your income. These plans adhere to specific quality standards and cover essential health benefits.

- Medicaid and CHIP: Medicaid and the Children’s Health Insurance Program (CHIP) provide free or low-cost coverage to low-income families and children. Eligibility is based on income and household size.

- Private Insurance Companies: Private insurance companies offer a wide variety of plans with varying coverage levels and deductibles. It’s important to compare quotes from multiple providers to find the best deal.

Choosing the Right Family Health Insurance Plan

When selecting a family health insurance plan, consider the following factors:

- Coverage Level: Choose a plan that meets your family’s specific needs, including coverage for doctor visits, hospital stays, and prescription drugs.

- Deductible: The deductible is the amount you pay out-of-pocket before the insurance coverage kicks in. Lower deductibles mean higher premiums, so find a balance that works for your budget.

- Coinsurance and Copayments: Coinsurance is a percentage of the cost you pay for covered services after meeting the deductible. Copayments are fixed amounts you pay for specific services like doctor visits or prescriptions.

- Provider Network: Make sure the plan includes doctors and hospitals you’re comfortable with. If you have specific healthcare providers you prefer, check if they’re covered under the plan.

Strategies to Get the Most Out of Your Family Health Insurance Plan

Once you have a family health insurance plan in place, there are several strategies you can employ to maximize its benefits:

1. Preventive Care:

Regular checkups, screenings, and vaccinations can help identify and address potential health issues early on, preventing costly treatments down the road. Preventive care is often covered by insurance, so take advantage of these services.

2. Generic Prescriptions:

When possible, opt for generic prescription drugs instead of brand-name ones. Generic drugs contain the same active ingredients and are just as effective, but they cost significantly less. Your insurance plan may offer generic medications at lower copayments.

3. In-Network Providers:

Staying within your plan’s provider network can save you money. When you receive care from in-network providers, your insurance plan has negotiated lower rates for services, resulting in lower out-of-pocket costs.

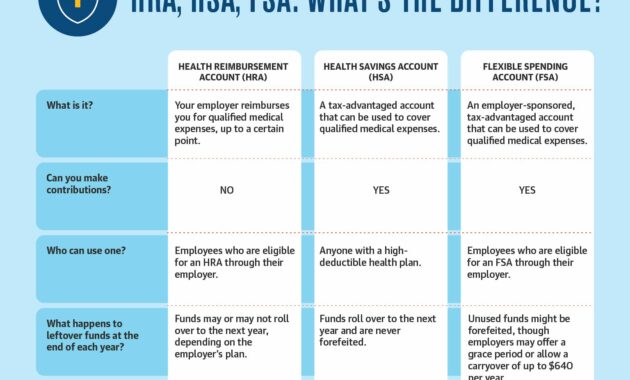

4. Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs):

FSAs and HSAs are tax-advantaged accounts that allow you to set aside pre-tax dollars to cover eligible healthcare expenses. FSAs can be used for a wider range of expenses than HSAs, but HSAs offer more investment options and can be carried over from year to year.

5. Take Advantage of Discounts:

Many insurance companies offer discounts for healthy behaviors like quitting smoking or joining a gym. Taking advantage of these incentives can reduce your premiums and save you money in the long run.

6. Review Your Coverage Regularly:

As your family’s needs change, so should your health insurance coverage. Review your plan annually to ensure it still meets your requirements. Consider changes in family size, income, and health status.

7. Communicate with Your Insurance Provider:

Don’t hesitate to reach out to your insurance provider if you have questions or concerns. They can provide guidance on coverage, benefits, and claims.

Conclusion

Finding an affordable family health insurance plan requires careful consideration and research. By understanding your options, choosing the right plan, and implementing strategies to maximize its benefits, you can secure comprehensive coverage that protects your family’s health and well-being without overburdening your budget.

Remember, investing in affordable health insurance is an investment in your family’s future. By planning ahead and making informed decisions, you can ensure that your loved ones have access to the healthcare they need when they need it most.

{kind=link}